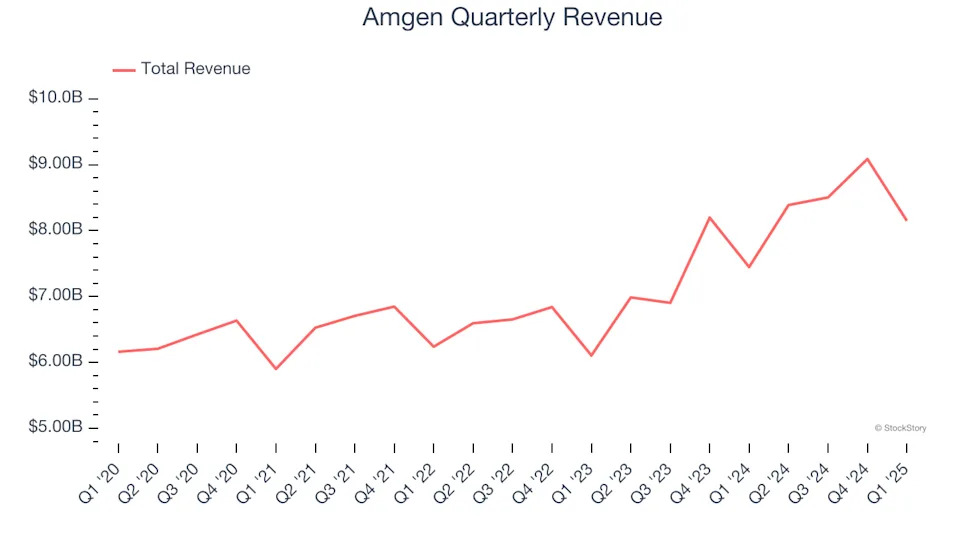

Biotech company Amgen (NASDAQ:AMGN) announced better-than-expected revenue in Q1 CY2025, with sales up 9.4% year on year to $8.15 billion. The company expects the full year’s revenue to be around $35 billion, close to analysts’ estimates. Its non-GAAP profit of $4.90 per share was 15% above analysts’ consensus estimates.

"Demand for our products was strong globally in the first quarter. Ongoing new product launches and successful Phase 3 trial results for several products make us feel confident in our long-term growth prospects," said Robert A. Bradway, chairman and CEO.

Company Overview

Founded in 1980 during the early days of the biotechnology revolution, Amgen (NASDAQ:AMGN) is a biotechnology company that discovers, develops, and manufactures innovative medicines to treat serious illnesses like cancer, osteoporosis, and autoimmune diseases.

Sales Growth

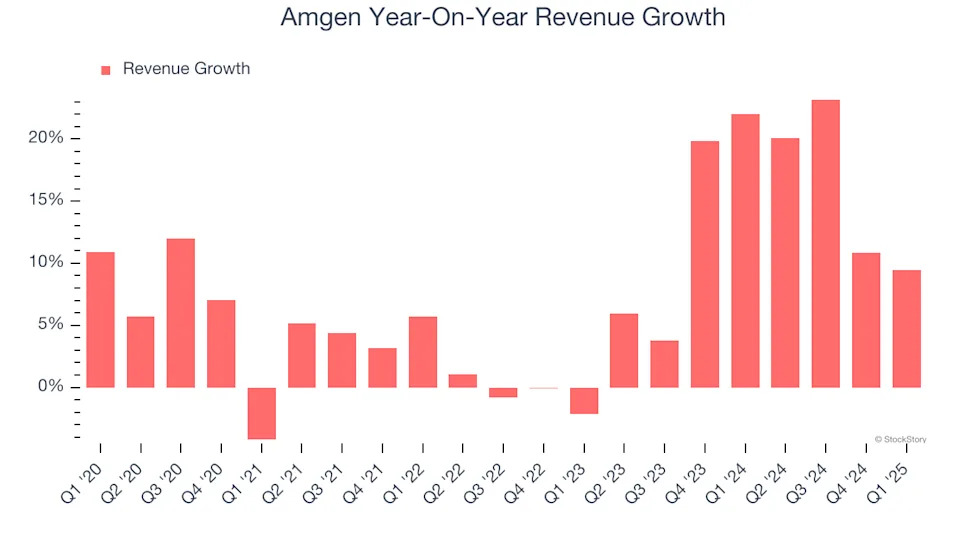

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Amgen grew its sales at a mediocre 7.3% compounded annual growth rate. This wasn’t a great result compared to the rest of the healthcare sector, but there are still things to like about Amgen.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Amgen’s annualized revenue growth of 14.1% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

Amgen also breaks out the revenue for its most important segment, Product & Pipeline. Over the last two years, Amgen’s Product & Pipeline revenue averaged 13.6% year-on-year growth.

This quarter, Amgen reported year-on-year revenue growth of 9.4%, and its $8.15 billion of revenue exceeded Wall Street’s estimates by 1.5%.

Looking ahead, sell-side analysts expect revenue to grow 3% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

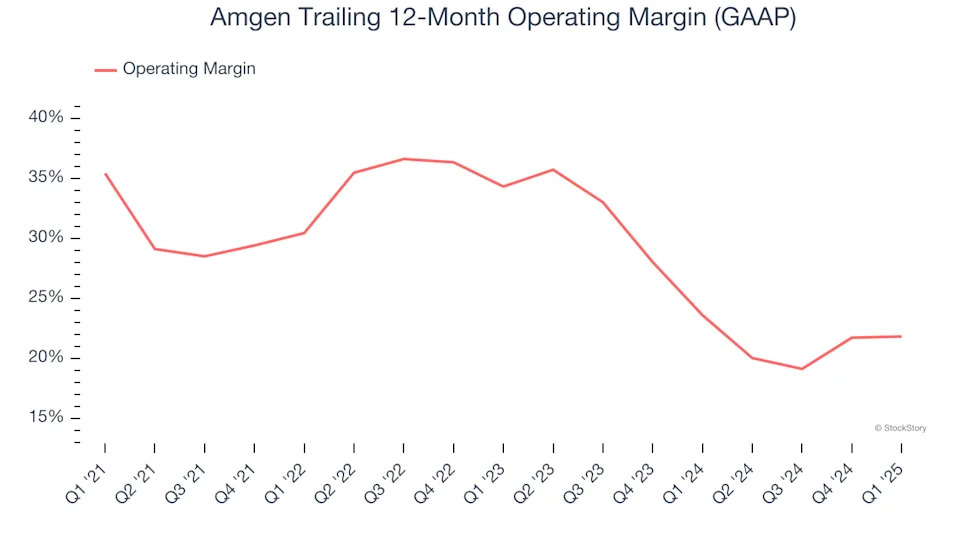

Amgen has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 28.5%.

Looking at the trend in its profitability, Amgen’s operating margin decreased by 13.6 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 12.5 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q1, Amgen generated an operating profit margin of 14.5%, up 1.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

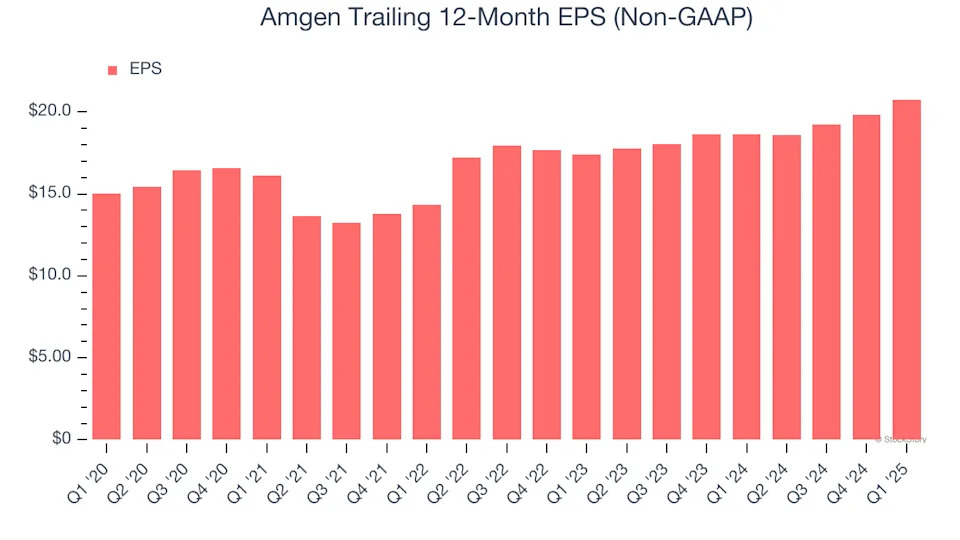

Amgen’s decent 6.7% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q1, Amgen reported EPS at $4.90, up from $3.96 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Amgen’s full-year EPS of $20.76 to stay about the same.

Key Takeaways from Amgen’s Q1 Results

We enjoyed seeing Amgen beat analysts’ revenue and EPS expectations this quarter. Overall, this print had some key positives. The stock remained flat at $284.80 immediately following the results.