Casella Waste Systems (NASDAQ:CWST) Beats Expectations in Strong Q1

May 1, 2025

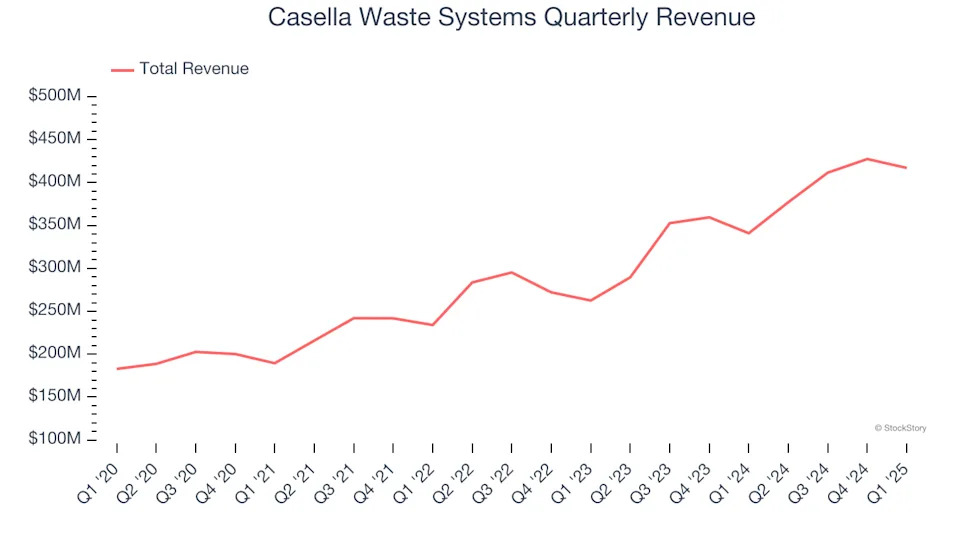

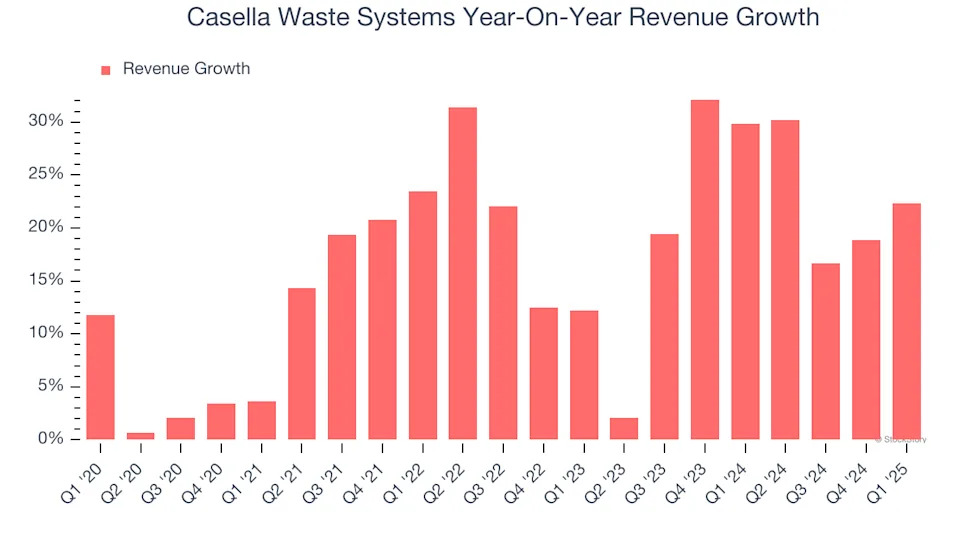

Waste management company Casella (NASDAQ:CWST) beat Wall Street’s revenue expectations in Q1 CY2025, with sales up 22.3% year on year to $417.1 million. The company expects the full year’s revenue to be around $1.79 billion, close to analysts’ estimates. Its non-GAAP profit of $0.19 per share was 85% above analysts’ consensus estimates.

Casella Waste Systems (CWST) Q1 CY2025 Highlights:

“We had a strong first quarter to start the year, with both revenue and Adjusted EBITDA up over 20% year-over-year, as we continue to execute successfully on our operating and growth strategies,” said John W. Casella, Chairman and CEO of Casella Waste Systems,

Company Overview

Starting with the founder picking up garbage with a pickup truck he purchased using savings from high school, Casella (NASDAQ:CWST) offers waste management services for businesses, residents, and the government.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Casella Waste Systems’s 16.5% annualized revenue growth over the last five years was incredible. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Casella Waste Systems’s annualized revenue growth of 21.1% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Casella Waste Systems reported robust year-on-year revenue growth of 22.3%, and its $417.1 million of revenue topped Wall Street estimates by 3.1%.

Looking ahead, sell-side analysts expect revenue to grow 11.7% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is admirable and suggests the market is forecasting success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming.

Click here to access a free report on our 3 favorite stocks to play this generational megatrend

.

Operating Margin

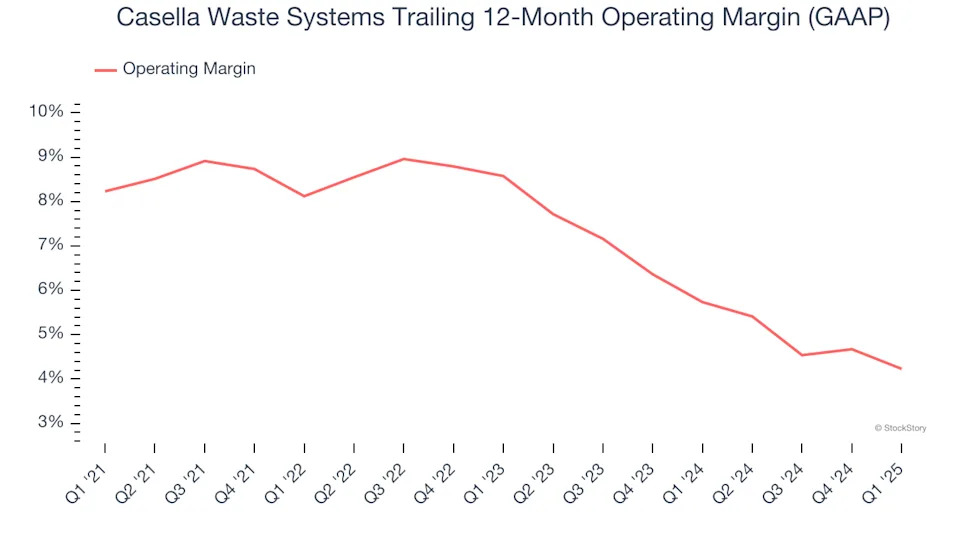

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Casella Waste Systems was profitable over the last five years but held back by its large cost base. Its average operating margin of 6.6% was weak for an industrials business. This result is surprising given its high gross margin as a starting point.

Analyzing the trend in its profitability, Casella Waste Systems’s operating margin decreased by 4 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Casella Waste Systems’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q1, Casella Waste Systems’s breakeven margin was down 1.3 percentage points year on year. Since Casella Waste Systems’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

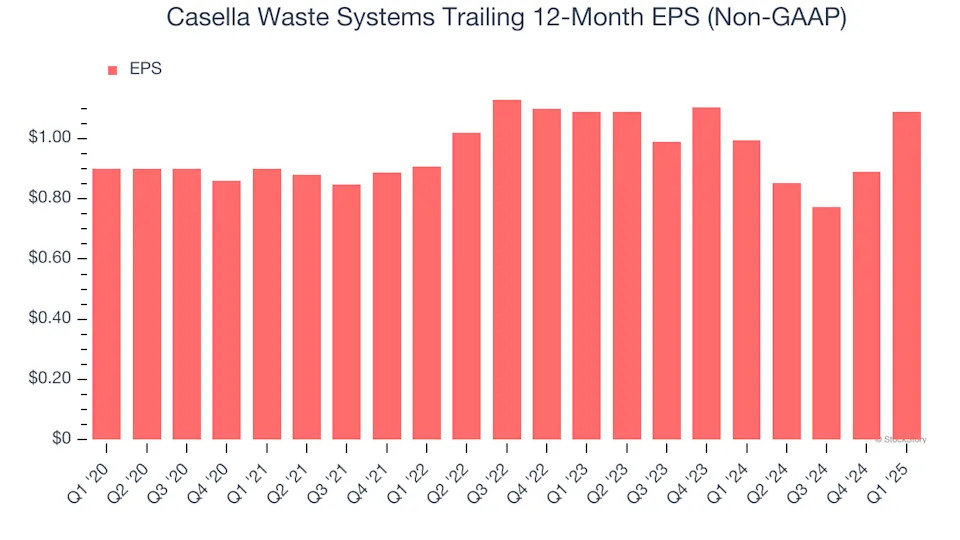

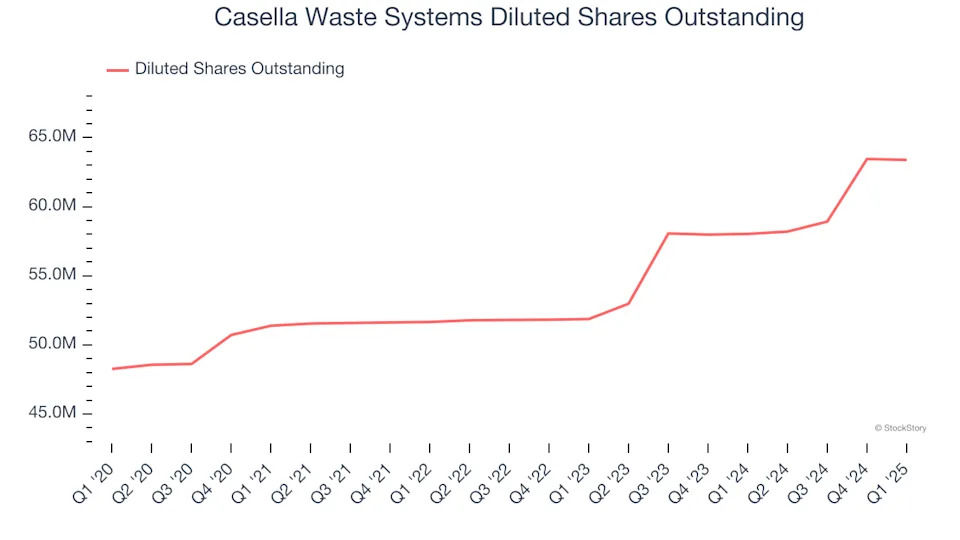

Casella Waste Systems’s EPS grew at a weak 3.9% compounded annual growth rate over the last five years, lower than its 16.5% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

We can take a deeper look into Casella Waste Systems’s earnings to better understand the drivers of its performance. As we mentioned earlier, Casella Waste Systems’s operating margin declined by 4 percentage points over the last five years. Its share count also grew by 31.3%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Casella Waste Systems, EPS didn’t budge over the last two years, a regression from its five-year trend. We hope it can revert to earnings growth in the coming years.

In Q1, Casella Waste Systems reported EPS at $0.19, up from negative $0.01 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Casella Waste Systems’s full-year EPS of $1.09 to grow 10.7%.

Key Takeaways from Casella Waste Systems’s Q1 Results

We were impressed by how significantly Casella Waste Systems blew past analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $116.75 immediately after reporting.