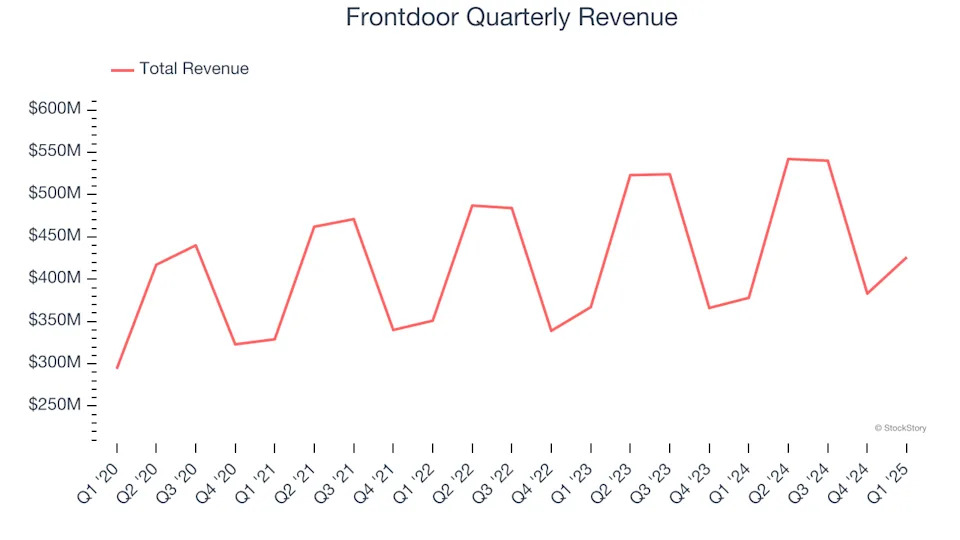

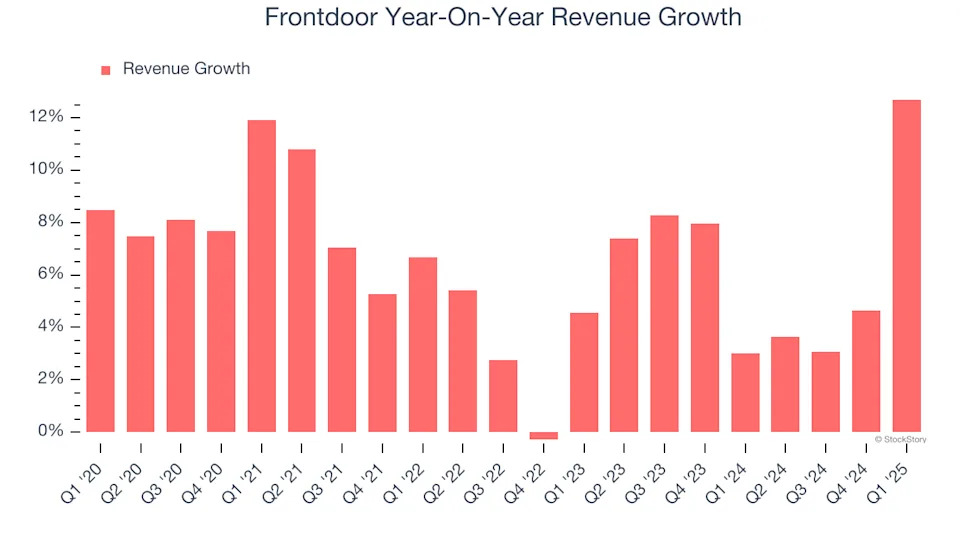

Home warranty company Frontdoor (NASDAQ:FTDR) announced better-than-expected revenue in Q1 CY2025, with sales up 12.7% year on year to $426 million. Guidance for next quarter’s revenue was better than expected at $602.5 million at the midpoint, 1.7% above analysts’ estimates. Its non-GAAP profit of $0.64 per share was 69.5% above analysts’ consensus estimates.

“We are off to a great start in 2025 and are pleased to increase our full-year outlook across the board," said Chairman and Chief Executive Officer Bill Cobb.

Company Overview

Established in 2018 as a spin-off from ServiceMaster Global Holdings, Frontdoor (NASDAQ:FTDR) is a provider of home warranty and service plans.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Frontdoor’s sales grew at a sluggish 6.4% compounded annual growth rate over the last five years. This fell short of our benchmark for the consumer discretionary sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Frontdoor’s annualized revenue growth of 6.2% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Frontdoor reported year-on-year revenue growth of 12.7%, and its $426 million of revenue exceeded Wall Street’s estimates by 2.1%. Company management is currently guiding for a 11.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.3% over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI.

Click here to access our free report one of our favorites growth stories

.

Operating Margin

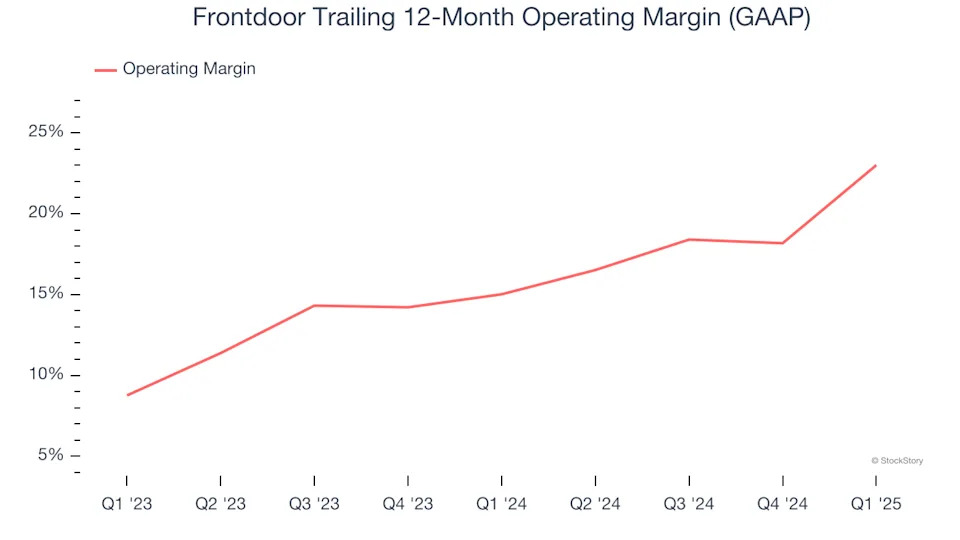

Frontdoor’s operating margin has been trending up over the last 12 months and averaged 19.1% over the last two years. On top of that, its profitability was top-notch for a consumer discretionary business, showing it’s an well-run company with an efficient cost structure.

In Q1, Frontdoor generated an operating profit margin of 35.4%, up 22 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

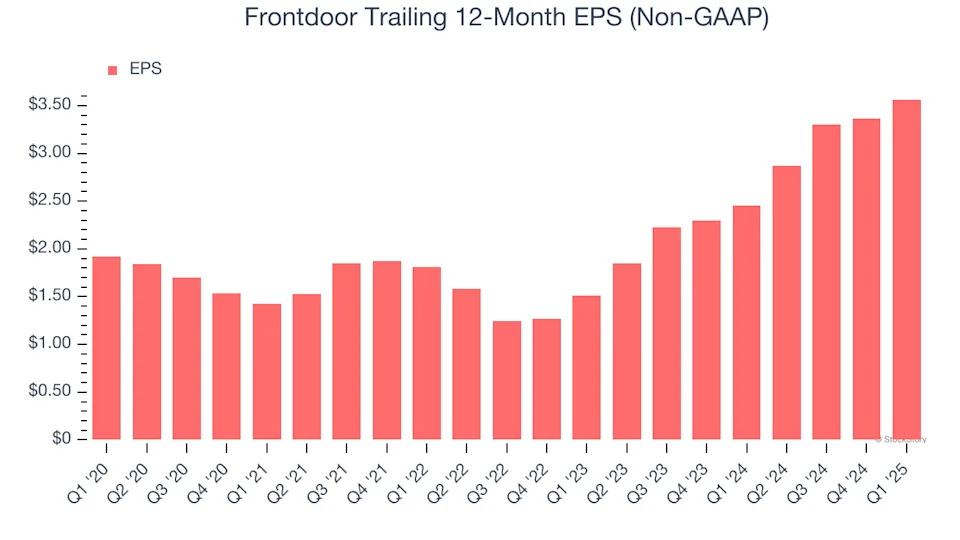

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Frontdoor’s EPS grew at a solid 13.2% compounded annual growth rate over the last five years, higher than its 6.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q1, Frontdoor reported EPS at $0.64, up from $0.44 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Frontdoor’s full-year EPS of $3.57 to shrink by 14.4%.

Key Takeaways from Frontdoor’s Q1 Results

This was a beat and raise quarter. We were impressed that the company raised full-year revenue guidance and also by Frontdoor’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its EPS outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 16.3% to $47.78 immediately after reporting.