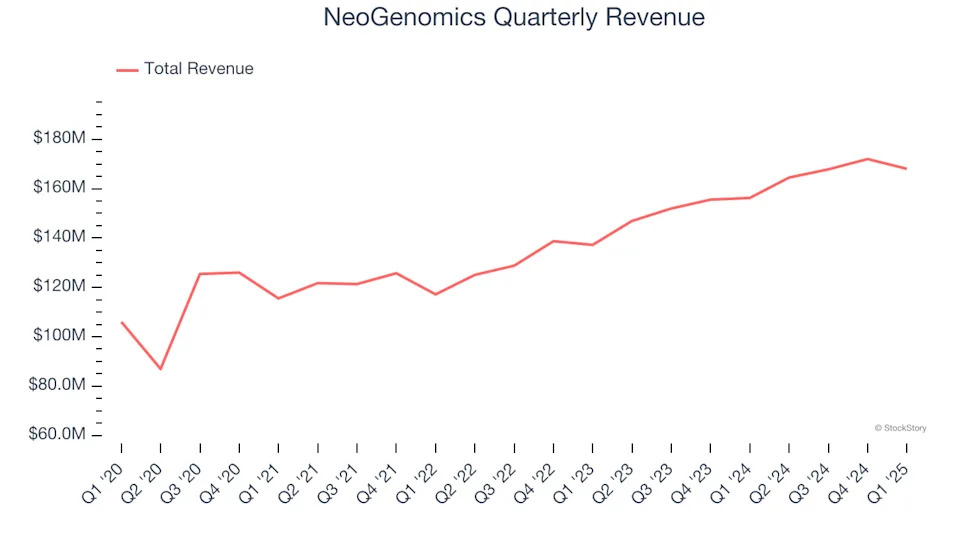

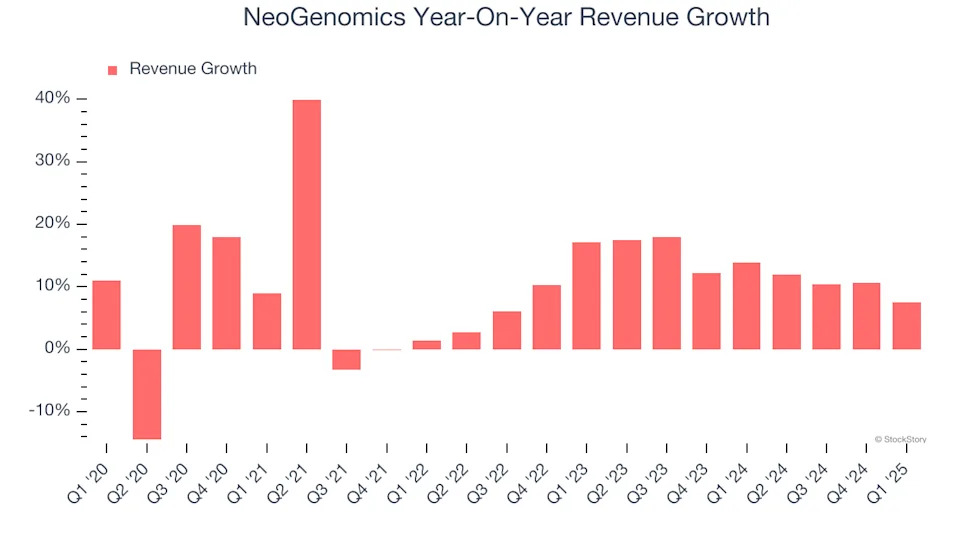

Oncology (cancer) diagnostics company NeoGenomics (NASDAQ:NEO) fell short of the market’s revenue expectations in Q1 CY2025, but sales rose 7.5% year on year to $168 million. On the other hand, the company’s full-year revenue guidance of $753 million at the midpoint came in 2% above analysts’ estimates. Its non-GAAP loss of $0 per share was in line with analysts’ consensus estimates.

“Our business is off to a solid start in 2025 with our team delivering a record number of results to patients in the first quarter and improving our adjusted EBITDA by over 100% from prior year,” said Tony Zook, CEO of NeoGenomics.

Company Overview

Operating a network of CAP-accredited and CLIA-certified laboratories across the United States and United Kingdom, NeoGenomics (NASDAQ:NEO) provides specialized cancer diagnostic testing services, including genetic analysis, molecular testing, and pathology consultation for oncologists and healthcare providers.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, NeoGenomics grew its sales at a decent 9.9% compounded annual growth rate. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. NeoGenomics’s annualized revenue growth of 12.7% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, NeoGenomics’s revenue grew by 7.5% year on year to $168 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 12.7% over the next 12 months, similar to its two-year rate. This projection is admirable and suggests the market is forecasting success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming.

Click here to access a free report on our 3 favorite stocks to play this generational megatrend

.

Operating Margin

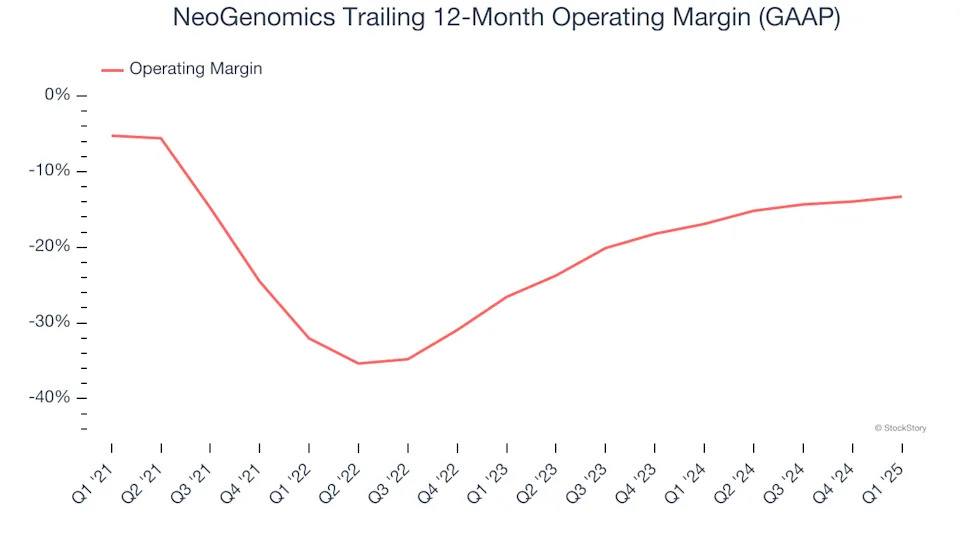

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

NeoGenomics’s high expenses have contributed to an average operating margin of negative 18.6% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, NeoGenomics’s operating margin decreased by 8 percentage points over the last five years, but it rose by 13.3 percentage points on a two-year basis. Still, shareholders will want to see NeoGenomics become more profitable in the future.

In Q1, NeoGenomics generated a negative 16.6% operating margin. The company's consistent lack of profits raise a flag.

Earnings Per Share

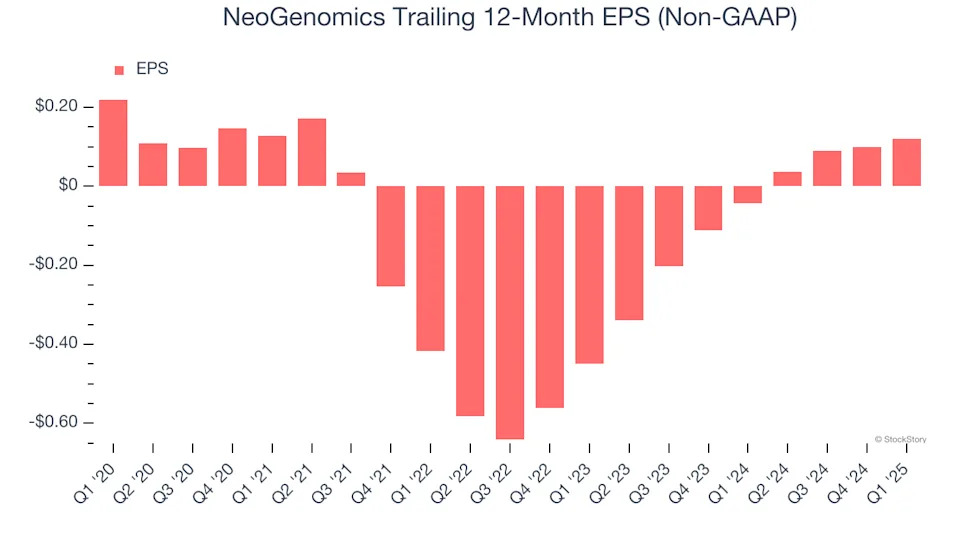

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for NeoGenomics, its EPS declined by 11.4% annually over the last five years while its revenue grew by 9.9%. This tells us the company became less profitable on a per-share basis as it expanded.

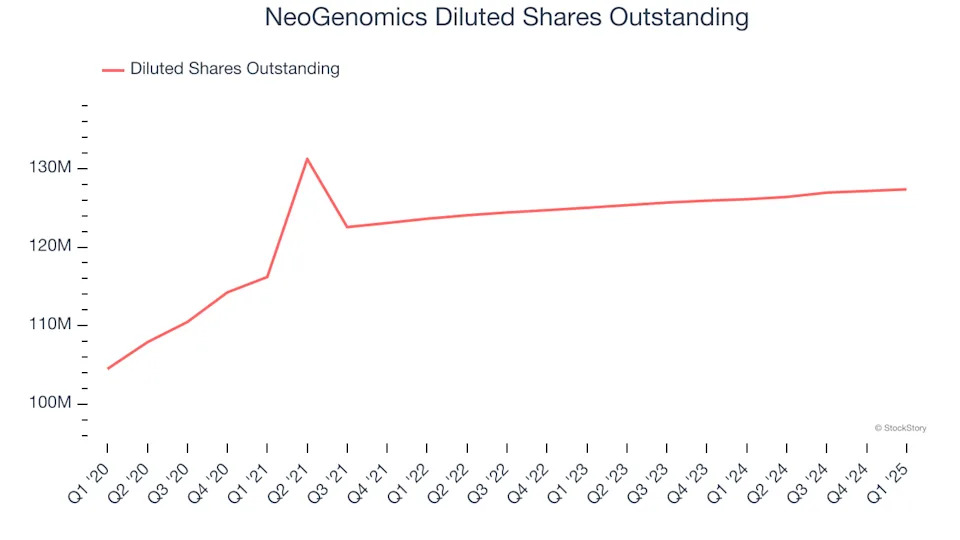

Diving into the nuances of NeoGenomics’s earnings can give us a better understanding of its performance. As we mentioned earlier, NeoGenomics’s operating margin improved this quarter but declined by 8 percentage points over the last five years. Its share count also grew by 21.9%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q1, NeoGenomics reported EPS at $0, up from negative $0.02 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects NeoGenomics to perform poorly. Analysts forecast its full-year EPS of $0.12 will hit $0.22.

Key Takeaways from NeoGenomics’s Q1 Results

We liked that NeoGenomics beat analysts’ EPS expectations this quarter. We were also glad its full-year revenue guidance exceeded Wall Street’s estimates. On the other hand, its revenue missed. Another blemish is that while full-year revenue guidance was raised, full-year EBITDA guidance was maintained, signaling that profit margins for the year will be lower than initially expected. Overall, this quarter was mixed. The areas below expectations seem to be driving the move, and shares traded down 7.2% to $9.25 immediately after reporting.