3 Reasons ACEL is Risky and 1 Stock to Buy Instead

Accel Entertainment trades at $10.28 per share and has stayed right on track with the overall market, losing 9.5% over the last six months while the S&P 500 is down 5.4%. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Accel Entertainment, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free .

Even with the cheaper entry price, we're swiping left on Accel Entertainment for now. Here are three reasons why there are better opportunities than ACEL and a stock we'd rather own.

Why Is Accel Entertainment Not Exciting?

Established in Illinois, Accel Entertainment (NYSE:ACEL) is a provider of electronic gaming machines and interactive amusement terminals to bars and entertainment venues.

1. Lackluster Revenue Growth

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Accel Entertainment’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 12.7% over the last two years was well below its five-year trend.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Accel Entertainment’s revenue to rise by 6.1%, a deceleration versus its 12.7% annualized growth for the past two years. This projection doesn't excite us and implies its products and services will face some demand challenges.

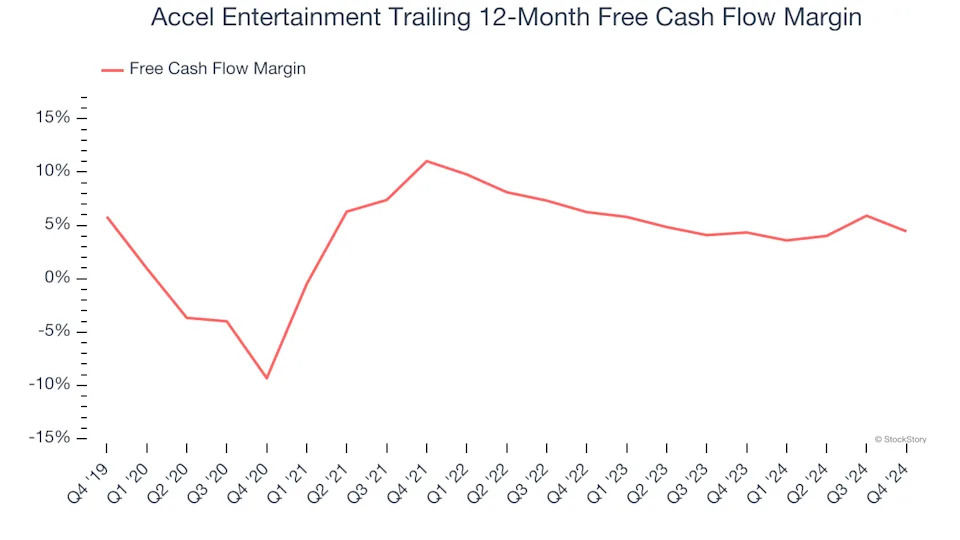

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Accel Entertainment has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.4%, lousy for a consumer discretionary business.

Final Judgment

Accel Entertainment isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 11.5× forward price-to-earnings (or $10.28 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere. Let us point you toward one of our top software and edge computing picks .