Lam Research (NASDAQ:LRCX) Beats Q1 Sales Targets, Provides Optimistic Revenue Guidance for Next Quarter

April 23, 2025

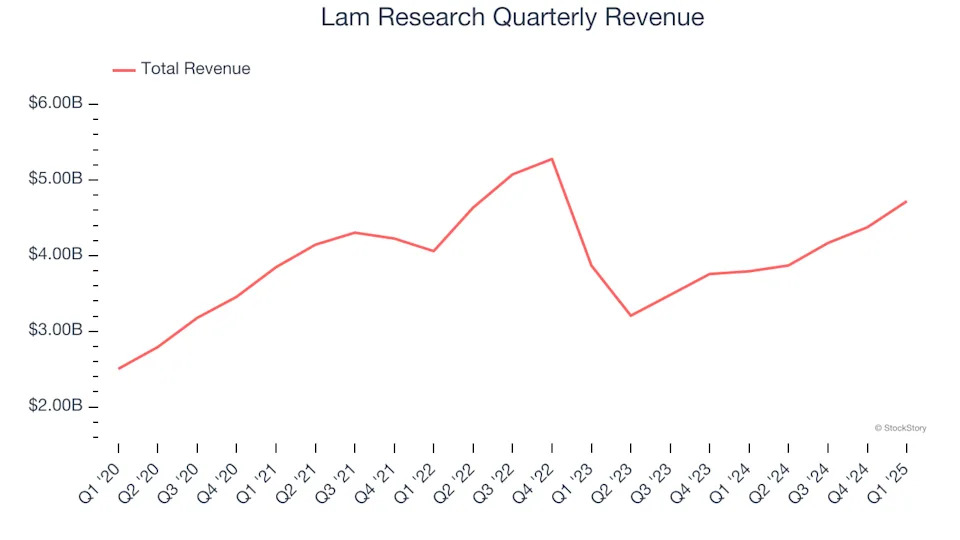

Semiconductor equipment maker Lam Research (NASDAQ:LRCX) reported revenue ahead of Wall Street’s expectations in Q1 CY2025, with sales up 24.4% year on year to $4.72 billion. On top of that, next quarter’s revenue guidance ($5 billion at the midpoint) was surprisingly good and 9.7% above what analysts were expecting. Its non-GAAP profit of $1.04 per share was 4.1% above analysts’ consensus estimates.

Founded in 1980 by David Lam, the man who pioneered semiconductor etching technology, Lam Research (NASDAQ:LRCX) is one of the leading providers of wafer fabrication equipment used to make semiconductors.

Semiconductor Manufacturing

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers, and data storage. The need for technologies like artificial intelligence, 5G networks, and smart cars is also creating the next wave of growth for the industry. Keeping up with this dynamism requires new tools that can design, fabricate, and test chips at ever smaller sizes and more complex architectures, creating a dire need for semiconductor capital manufacturing equipment.

Sales Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Lam Research’s 12.3% annualized revenue growth over the last five years was solid. Its growth beat the average semiconductor company and shows its offerings resonate with customers, a helpful starting point for our analysis. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Lam Research’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 4.7% over the last two years.

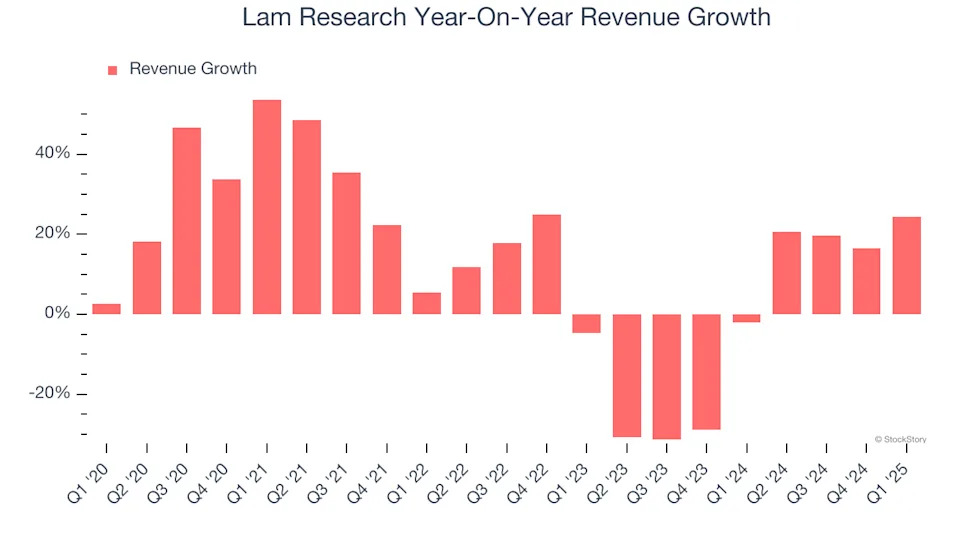

This quarter, Lam Research reported robust year-on-year revenue growth of 24.4%, and its $4.72 billion of revenue topped Wall Street estimates by 1.7%. Beyond the beat, this marks 4 straight quarters of growth, implying that Lam Research is in the middle of its cycle - a typical upcycle generally lasts 8-10 quarters. Company management is currently guiding for a 29.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.9% over the next 12 months. Although this projection implies its newer products and services will catalyze better top-line performance, it is still below the sector average. At least the company is tracking well in other measures of financial health.

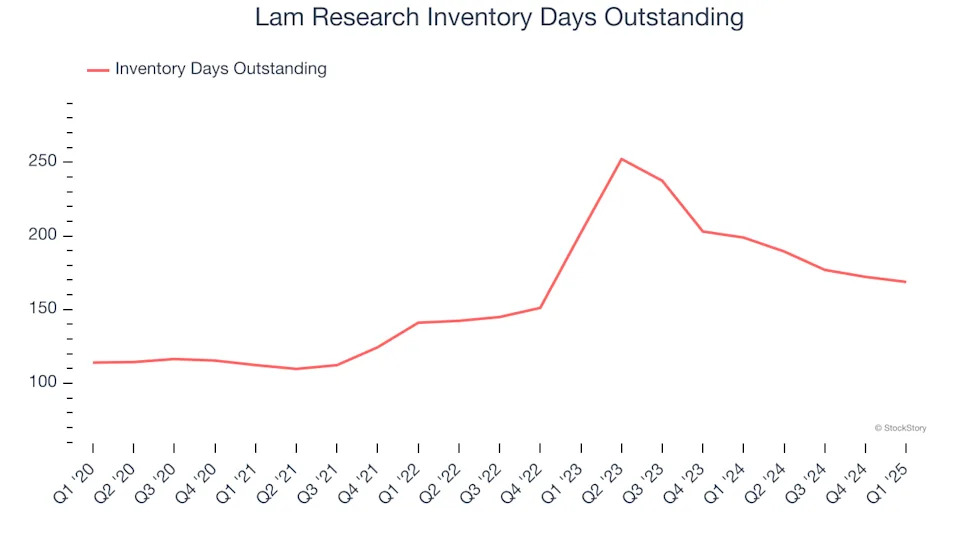

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Lam Research’s DIO came in at 169, which is 9 days above its five-year average. These numbers suggest that despite the recent decrease, the company’s inventory levels are higher than what we’ve seen in the past.

Key Takeaways from Lam Research’s Q1 Results

We were impressed by Lam Research’s optimistic revenue guidance for next quarter, which blew past analysts’ expectations. We were also glad its adjusted operating income outperformed Wall Street’s estimates. Zooming out, we think this was a good quarter with some key areas of upside. The stock traded up 4.7% to $69.75 immediately after reporting.