3 Reasons to Avoid SKIN and 1 Stock to Buy Instead

Shareholders of BeautyHealth would probably like to forget the past six months even happened. The stock dropped 46.5% and now trades at $0.89. This may have investors wondering how to approach the situation.

Is there a buying opportunity in BeautyHealth, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free .

Even with the cheaper entry price, we're cautious about BeautyHealth. Here are three reasons why we avoid SKIN and a stock we'd rather own.

Why Do We Think BeautyHealth Will Underperform?

Operating in the emerging beauty health category, the appropriately named BeautyHealth (NASDAQ:SKIN) is a skincare company best known for its Hydrafacial product that cleanses and hydrates skin.

1. Fewer Distribution Channels Limit its Ceiling

With $334.3 million in revenue over the past 12 months, BeautyHealth is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

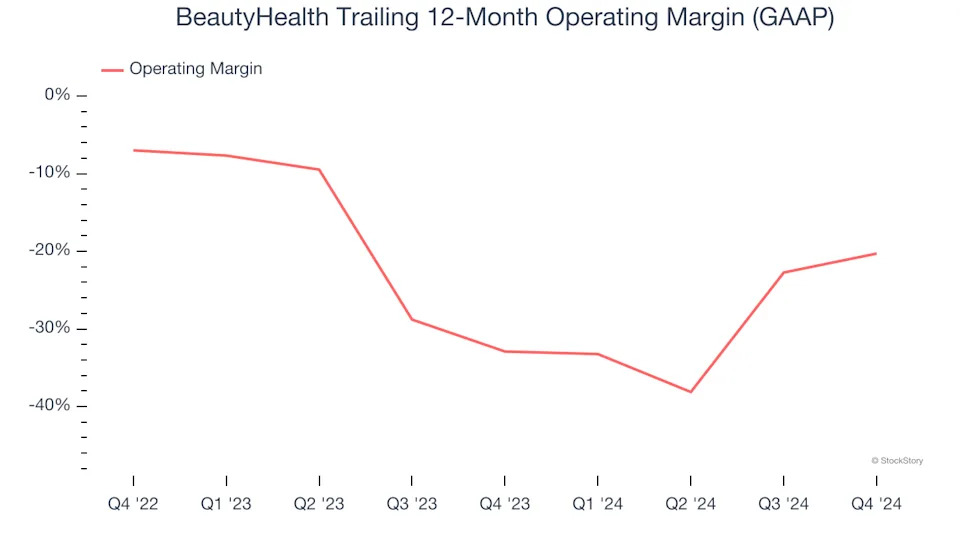

2. Operating Losses Sound the Alarms

Operating margin is a key profitability metric because it accounts for all expenses enabling a business to operate smoothly, including marketing and advertising, IT systems, wages, and other administrative costs.

Unprofitable public companies are rare in the defensive consumer staples industry. Unfortunately, BeautyHealth was one of them over the last two years as its high expenses contributed to an average operating margin of negative 27.1%.

3. High Debt Levels Increase Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

BeautyHealth’s $557.3 million of debt exceeds the $370.1 million of cash on its balance sheet. Furthermore, its 15× net-debt-to-EBITDA ratio (based on its EBITDA of $12.3 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. BeautyHealth could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope BeautyHealth can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.