3 Reasons to Sell GDRX and 1 Stock to Buy Instead

GoodRx’s stock price has taken a beating over the past six months, shedding 30.4% of its value and falling to $4.55 per share. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in GoodRx, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free .

Even though the stock has become cheaper, we're cautious about GoodRx. Here are three reasons why we avoid GDRX and a stock we'd rather own.

Why Do We Think GoodRx Will Underperform?

Started in 2011 to tackle the problem of high prescription drug costs in America, GoodRx (NASDAQ:GDRX) operates a digital platform that helps consumers find lower prices on prescription medications through price comparison tools and discount codes.

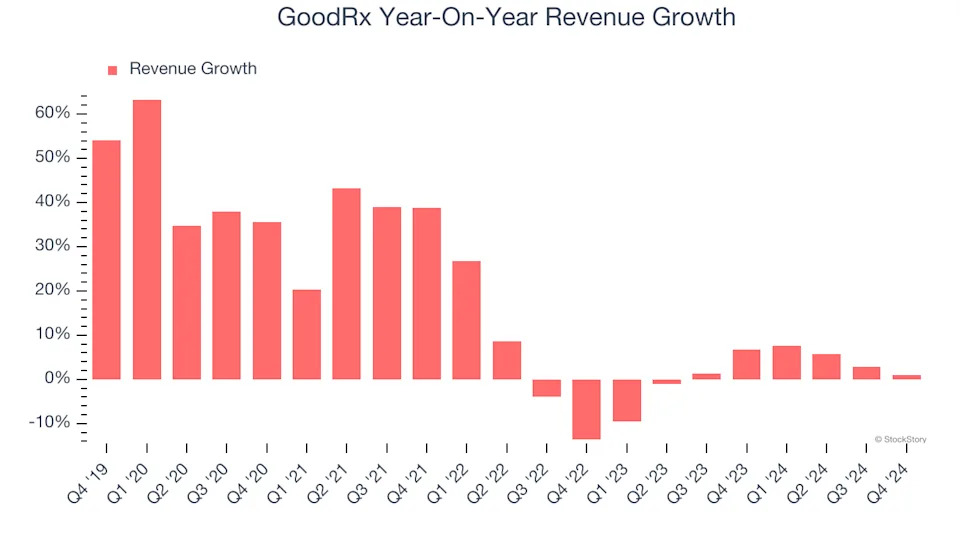

1. Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within healthcare, a stretched historical view may miss recent innovations or disruptive industry trends. GoodRx’s recent performance shows its demand has slowed as its annualized revenue growth of 1.7% over the last two years was below its five-year trend.

2. Fewer Distribution Channels Limit its Ceiling

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $792.3 million in revenue over the past 12 months, GoodRx is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

3. Previous Growth Initiatives Have Lost Money

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

GoodRx’s five-year average ROIC was negative 3.7%, meaning management lost money while trying to expand the business. Its returns were among the worst in the healthcare sector.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of GoodRx, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 10.7× forward price-to-earnings (or $4.55 per share). At this valuation, there’s a lot of good news priced in - you can find better investment opportunities elsewhere. We’d suggest looking at the most dominant software business in the world .