3 Reasons to Sell ODFL and 1 Stock to Buy Instead

Shareholders of Old Dominion Freight Line would probably like to forget the past six months even happened. The stock dropped 25.8% and now trades at $151.05. This may have investors wondering how to approach the situation.

Is now the time to buy Old Dominion Freight Line, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free .

Even with the cheaper entry price, we're cautious about Old Dominion Freight Line. Here are three reasons why there are better opportunities than ODFL and a stock we'd rather own.

Why Is Old Dominion Freight Line Not Exciting?

With its name deriving from the Commonwealth of Virginia’s nickname, Old Dominion (NASDAQ:ODFL) delivers less-than-truckload (LTL) and full-container load freight.

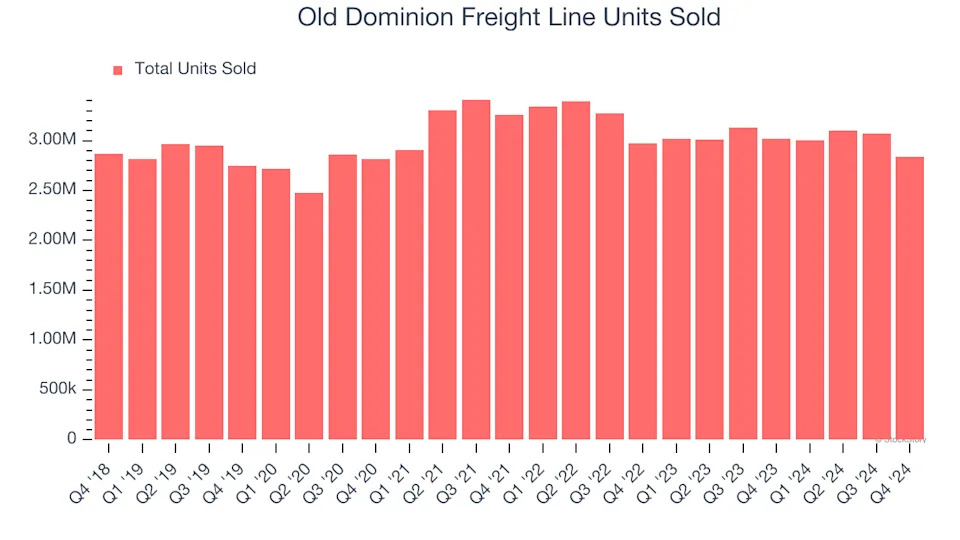

1. Demand Slipping as Sales Volumes Decline

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Ground Transportation company because there’s a ceiling to what customers will pay.

Old Dominion Freight Line’s units sold came in at 2.84 million in the latest quarter, and they averaged 3.7% year-on-year declines over the last two years. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Old Dominion Freight Line might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Old Dominion Freight Line’s revenue to stall. Although this projection implies its newer products and services will catalyze better top-line performance, it is still below the sector average.

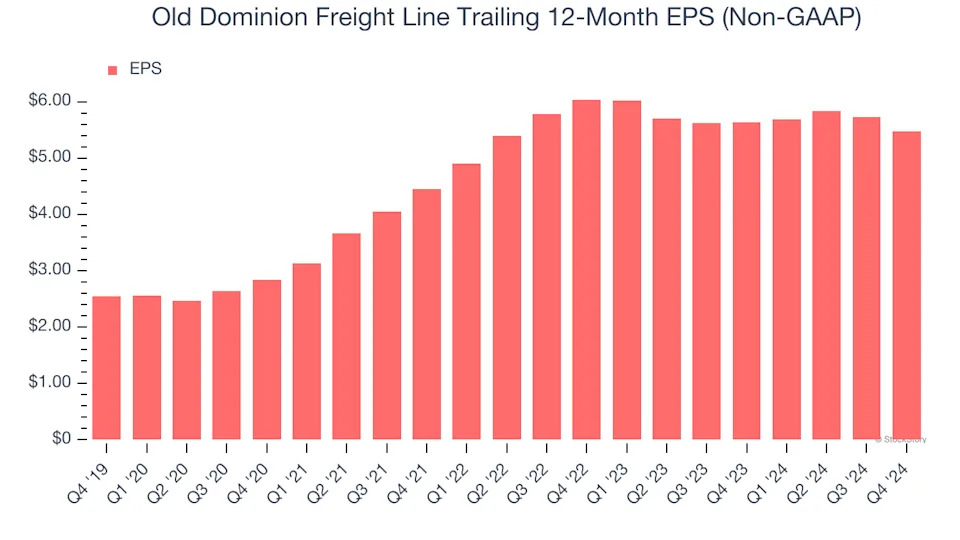

3. EPS Took a Dip Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Old Dominion Freight Line, its EPS declined by more than its revenue over the last two years, dropping 4.7%. This tells us the company struggled to adjust to shrinking demand.

Final Judgment

Old Dominion Freight Line isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 27× forward price-to-earnings (or $151.05 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. Let us point you toward our favorite semiconductor picks and shovels play .