3 Reasons to Avoid FCN and 1 Stock to Buy Instead

FTI Consulting’s stock price has taken a beating over the past six months, shedding 26.5% of its value and falling to $164.61 per share. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy FTI Consulting, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free .

Even with the cheaper entry price, we're swiping left on FTI Consulting for now. Here are three reasons why you should be careful with FCN and a stock we'd rather own.

Why Is FTI Consulting Not Exciting?

With a team of experts deployed across 30+ countries to tackle complex business challenges, FTI Consulting (NYSE:FCN) is a global business advisory firm that helps organizations manage change, mitigate risk, and resolve disputes across financial, legal, operational, and regulatory matters.

1. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect FTI Consulting’s revenue to stall, a deceleration versus its 10.5% annualized growth for the past two years. This projection doesn't excite us and implies its products and services will face some demand challenges.

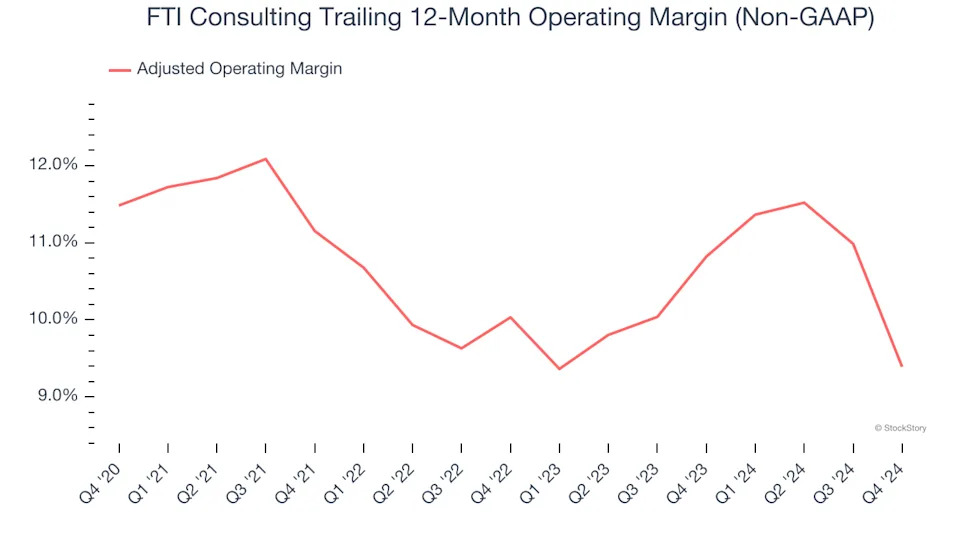

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Analyzing the trend in its profitability, FTI Consulting’s adjusted operating margin decreased by 2.1 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its adjusted operating margin for the trailing 12 months was 9.4%.

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, FTI Consulting’s margin dropped by 2.1 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal it is in the middle of an investment cycle. FTI Consulting’s free cash flow margin for the trailing 12 months was 9.7%.