3 Reasons to Avoid VNT and 1 Stock to Buy Instead

Vontier has followed the market’s trajectory closely. The stock is down 10.4% to $30.36 per share over the past six months while the S&P 500 has lost 7.8%. This may have investors wondering how to approach the situation.

Is now the time to buy Vontier, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free .

Even though the stock has become cheaper, we're cautious about Vontier. Here are three reasons why you should be careful with VNT and a stock we'd rather own.

Why Do We Think Vontier Will Underperform?

A spin-off of a spin-off, Vontier (NYSE:VNT) provides electronic products and systems to the transportation, automotive, and manufacturing sectors.

1. Core Business Falling Behind as Demand Plateaus

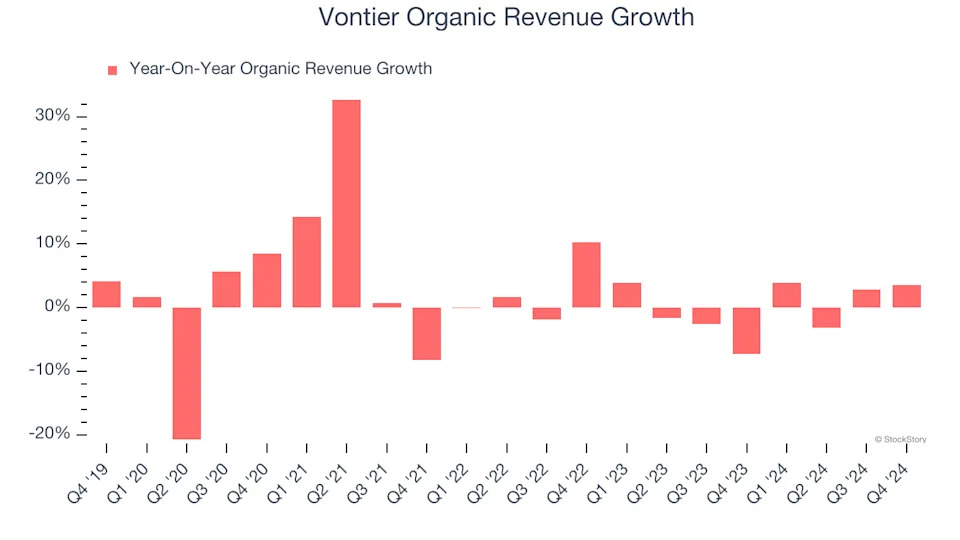

In addition to reported revenue, organic revenue is a useful data point for analyzing Internet of Things companies. This metric gives visibility into Vontier’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Vontier failed to grow its organic revenue. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests Vontier might have to lean into acquisitions to accelerate growth, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

2. Free Cash Flow Margin Dropping

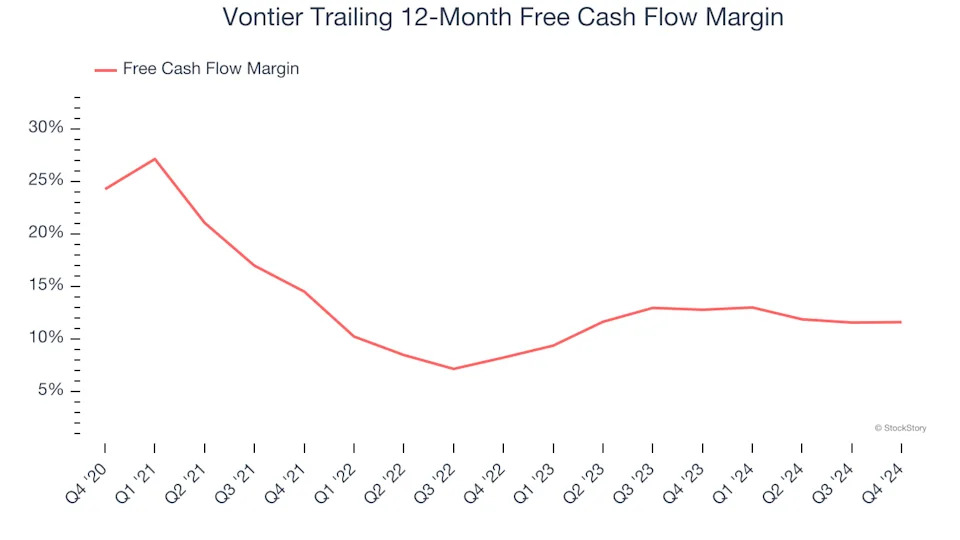

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Vontier’s margin dropped by 12.7 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Vontier’s free cash flow margin for the trailing 12 months was 11.6%.

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Vontier’s ROIC has unfortunately decreased significantly. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.