The first quarter of 2025 ended March 31. Now come the first earning reports of the new year as well as guidance for the remainder of the year. The first quarter didn’t see a lot of action with tariffs. There was a brief 48 hours during which the 25% tariffs on Canada and Mexico were in effect, but most everything was pushed off to the last week of March or the beginning of April.

Now that tariffs are in place on imports from every country in the world, it stands to be one of the spicier earnings seasons. No doubt some version of the same question will be asked on every earnings call: “How do you anticipate handling the impact of tariffs on the business?”

The mode that could be hit hardest is the less-than-truckload segment.

After the April 2 “Liberation Day,” where President Donald Trump announced the tariff plan, LTL stocks fell 18%. They are off 33% on a year-over-year basis.

As Todd Maiden wrote for

FreightWaves

: “The sector was a pandemic and post-pandemic darling, garnering record valuations at times, given its manufacturing-heavy exposure and role in a mass inventory restocking. However, an extended industrial downturn along with several carriers acquiring terminals from defunct Yellow Corp. in addition to other organic additions, has left many LTL networks at or near record latent capacity. That has LTL bears calling for an unraveling of the industry’s favorable pricing dynamics.”

Old Dominion has widely served as the bellwether for the LTL industry, setting the tone for what to expect for carriers in the market. Its earnings call is April 23. Following the Liberation Day announcement, its

stock price

was down 10.6% or 13.8% year to date. The other big players are much worse off, with Forward air taking the biggest hit, down 59.3% YTD.

It’s looking grim for the LTL sector, and those like TFI International that plan to overhaul operations are in for a rough first half of the year as volumes continues to evaporate from the market.

Working to stay ahead of disruptions, shippers were importing goods at a higher pace to mitigate as much of the cost impact as they could before mass tariffs went into effect. That was evident in the

Manufacturing Purchasing Managers’ Index

, which measures economic trends in the manufacturing and service sectors to understand their health and the level of new orders. Manufacturers saw growth in January and February as an effort to stay ahead of the impending tariffs, as data from March showed the market back in a contraction, ending the short-lived hope that orders would be strong for the year.

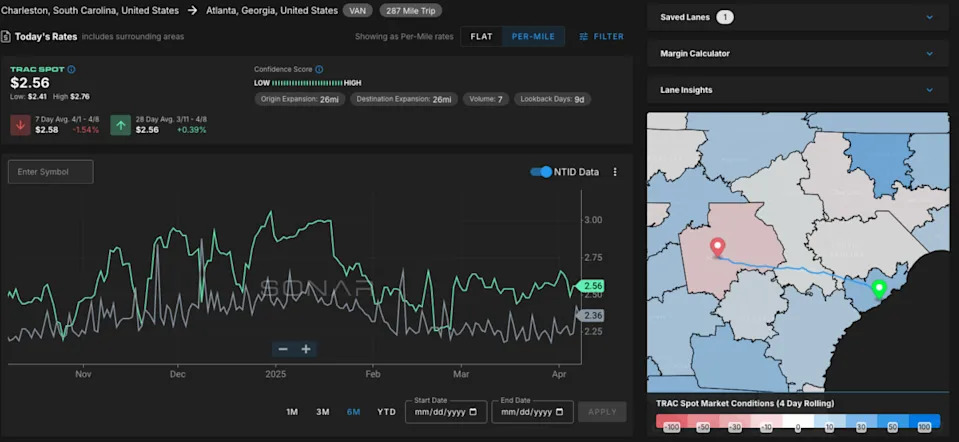

TRAC Tuesday.

This week’s TRAC lane goes from Charleston, South Carolina, to Atlanta – from a port to a major freight hub. It’s a lane that stands to be dramatically impacted as tariffs continue to reign. The

top import categories

for the port are furniture, sporting goods and toys, which account for 9.7% of goods or over 191,000 twenty-foot equivalent units. Those are all industries that are likely going to have reduced volumes as a result of tariffs – which leads to lower spot rates and more readily available capacity in major port markets.

As for the next few weeks until volumes level out, spot rates are still slightly elevated at $2.56 a mile compared to the National Truckload Index of $2.36 a mile. Capacity still has moderate availability in Atlanta and Charleston, with both markets seeing about 1% deviation in outbound tender rejections week over week. Two relatively stable markets face some likely disruption as tariffs continue on.

Who’s with whom

. The Panama Canal’s

dry season runs

from January to May. During this season, Lake Gatún, the lake that serves as the water reservoir for the canal, has lower-than-normal water levels, which can result in delays for ships traveling through the canal. While that was a massive issue in 2024, it’s seeming less of an issue for 2025.

Although the water levels aren’t affecting the flow of goods, there have been proposals for a new owner of some operations at the canal. The asset management giant BlackRock has agreed to buy two ports at either end of the Panama Canal from a Hong Kong-based firm. According to

CNN

, BlackRock and other investors plan to spend nearly $23 billion to buy the ports of Balboa and Cristobal from Hong Kong’s CK Hutchison. It said the deal is an “agreement in principle.”

Making a move of its own is APM Terminals, the rail arm of the ocean container giant Maersk. APM Terminals

has acquired

Panama Canal Railway Co. from Canadian Pacific Kansas City Ltd. and the Lanco Group/Mi‑Jack. This rail line connects the Atlantic and Pacific oceans. Financial terms of the deal were not disclosed. The route can serve as an alternative to the canal. Should the drought get worse for Lake Gatún or other geopolitical factors come into play, Maersk will see little interruption of service.

Keith Svendson, CEO of APM Terminals, said in a

news release

: “The Panama Canal Railway Company represents an attractive infrastructure investment in the region aligned to our core services of intermodal container movement. The company is highly regarded for its operational excellence and will provide a significant opportunity for us to offer a broader range of services to the global shipping customers we serve.”