Office furniture manufacturer MillerKnoll (NASDAQ:MLKN) missed Wall Street’s revenue expectations in Q1 CY2025, with sales flat year on year at $876.2 million. Next quarter’s revenue guidance of $930 million underwhelmed, coming in 3% below analysts’ estimates. Its non-GAAP profit of $0.44 per share was in line with analysts’ consensus estimates.

Created through the 2021 merger of industry icons Herman Miller and Knoll, MillerKnoll (NASDAQ:MLKN) designs, manufactures, and distributes interior furnishings for offices, healthcare facilities, educational settings, and homes worldwide.

Office & Commercial Furniture

The sector faces a tepid outlook as workplace dynamics continue to evolve. Hybrid work means that enterprise demand for office furniture is lower. Consumer demand for the same products likely will not offset the loss from enterprises, as individual workers tend to have less space and need for the sector's wares. The Trump administration also possesses a high willingness to impose tariffs on key partners, which could result in retaliatory actions, all of which could pressure those selling furniture that may feature components or labor from overseas. Lastly, the COVID-19 pandemic showed that there is always a risk that something disrupts supply chains, and companies need contingency plans for this.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

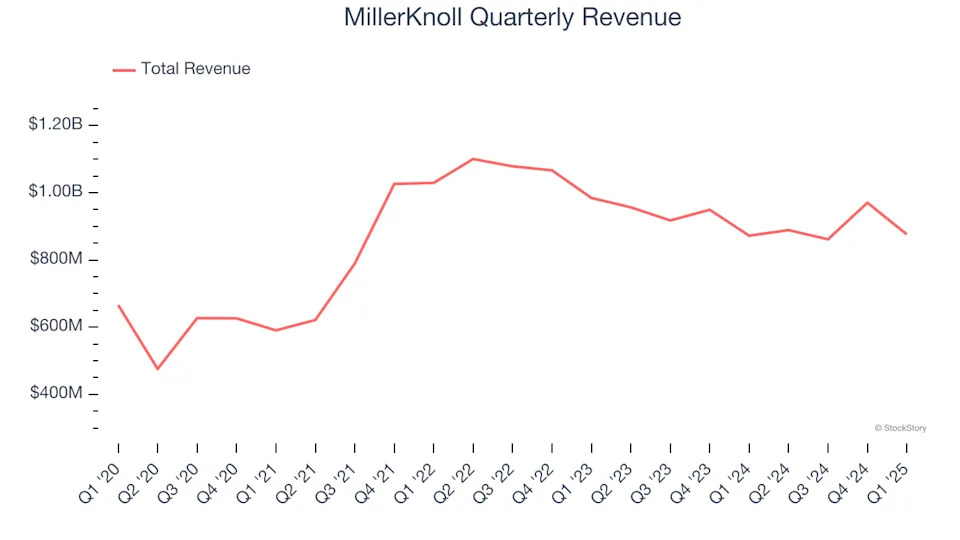

With $3.60 billion in revenue over the past 12 months, MillerKnoll is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

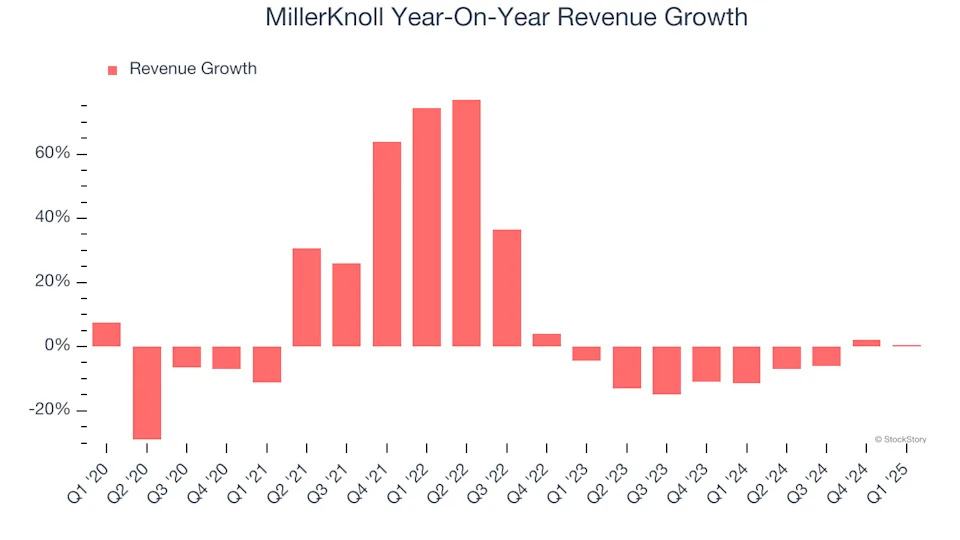

As you can see below, MillerKnoll grew its sales at a decent 6% compounded annual growth rate over the last five years. This shows its offerings generated slightly more demand than the average business services company, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. MillerKnoll’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 7.8% over the last two years.

This quarter, MillerKnoll’s $876.2 million of revenue was flat year on year, falling short of Wall Street’s estimates. Company management is currently guiding for a 4.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 7% over the next 12 months, an improvement versus the last two years. This projection is healthy and implies its newer products and services will spur better top-line performance.

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

MillerKnoll was profitable over the last five years but held back by its large cost base. Its average operating margin of 5% was weak for a business services business.

Analyzing the trend in its profitability, MillerKnoll’s operating margin decreased by 7.5 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. MillerKnoll’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, MillerKnoll generated an operating profit margin of negative 9.4%, down 15.4 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

Earnings Per Share

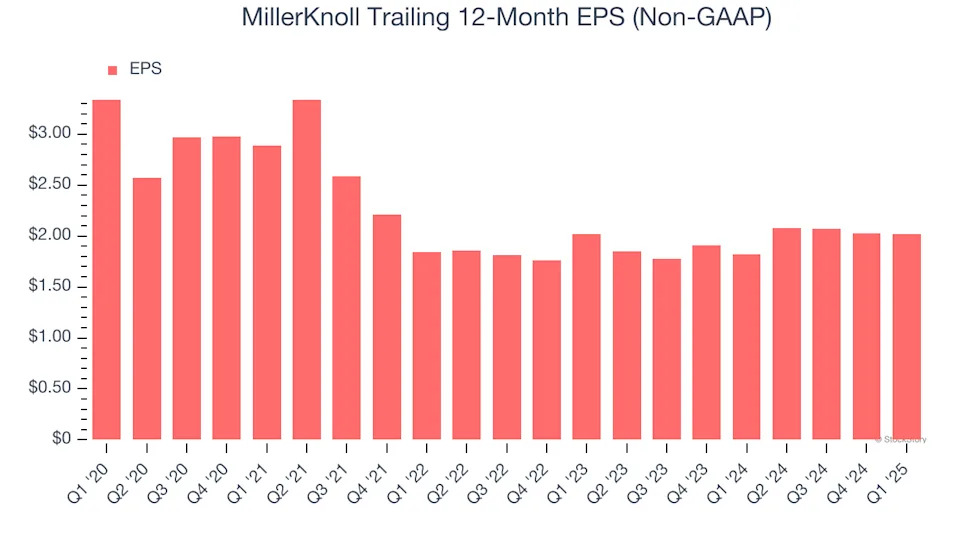

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for MillerKnoll, its EPS declined by 9.6% annually over the last five years while its revenue grew by 6%. This tells us the company became less profitable on a per-share basis as it expanded.

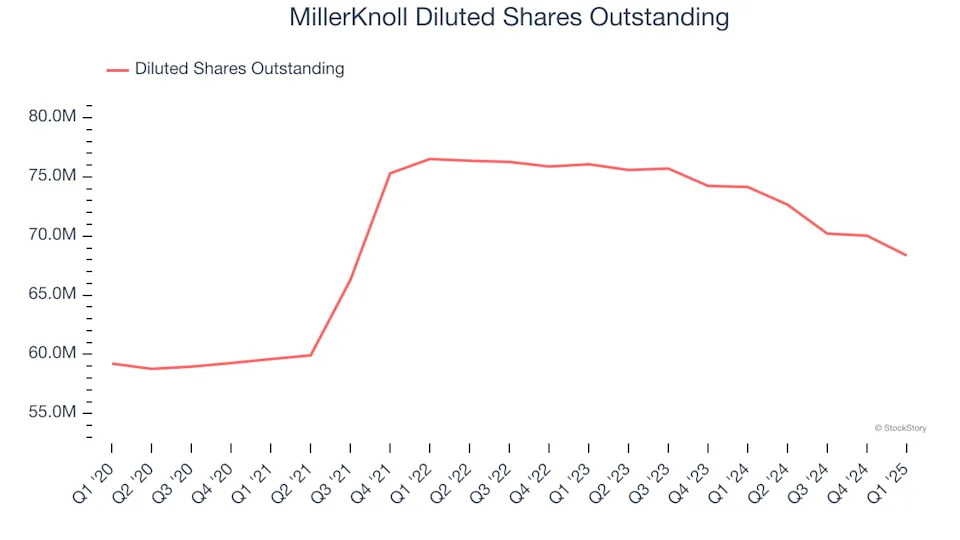

We can take a deeper look into MillerKnoll’s earnings to better understand the drivers of its performance. As we mentioned earlier, MillerKnoll’s operating margin declined by 7.5 percentage points over the last five years. Its share count also grew by 15.4%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q1, MillerKnoll reported EPS at $0.44, down from $0.45 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 1.1%. Over the next 12 months, Wall Street expects MillerKnoll’s full-year EPS of $2.02 to grow 22.1%.

Key Takeaways from MillerKnoll’s Q1 Results

We struggled to find many positives in these results. Its full-year EPS guidance missed significantly and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 3.3% to $17.74 immediately following the results.