Like most people who invest in the stock market,

I too get nervous

when prices are going down. When the selling gets protracted, muscle knots sometimes form in my neck and upper back.

To be clear,

I do not trade actively much at all

. But on rare occasions outside of regular periodic contributions to my retirement accounts, I’ve had the good fortune of having some extra cash to put to work.

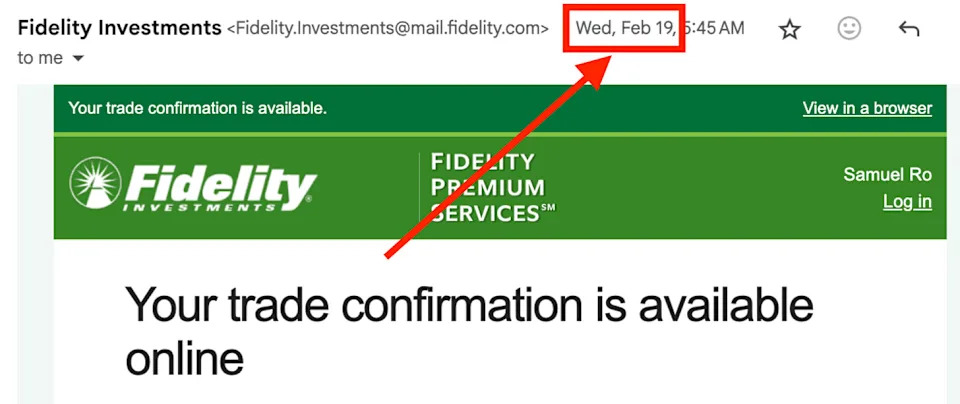

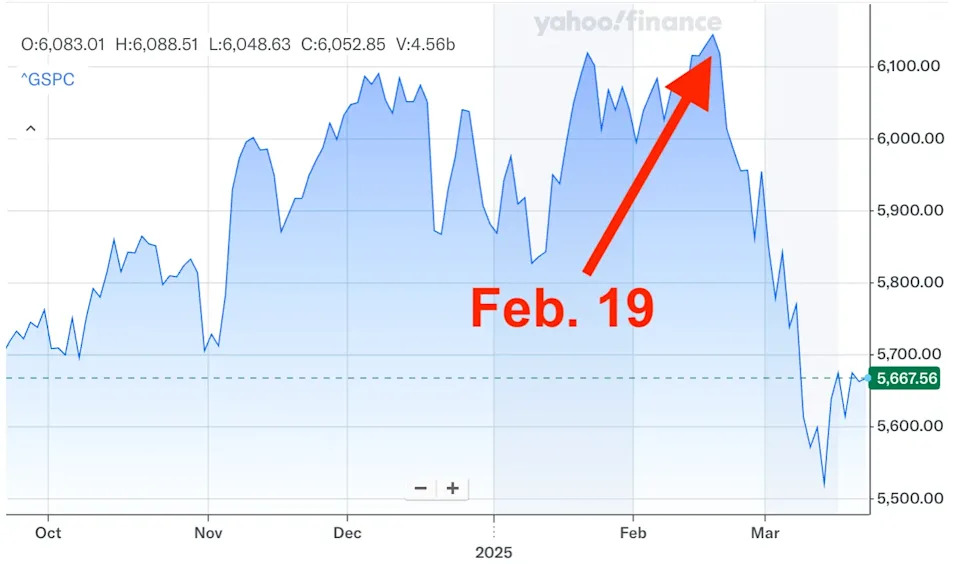

Wasting no time, I transferred cash to that account. And on Feb. 18, I added to my S&P 500 index fund position. The trade confirmation came in on Feb. 19.

Coincidentally, Feb. 19 was when the S&P 500 last touched a record high before rapidly tumbling into the correction we are living today.

Time is the unlucky market timer’s best friend ⏱️

This is not the first time I found myself with some cash to put to work.

As I wrote in the

March 6, 2022 TKer

, I faced similar situations in late 2015 and late 2021. Both times, I made lump sum purchases into S&P 500 index funds.

And both times, those purchases were almost immediately followed by steep sell-offs.

The 2015 purchase happened while the S&P was on the precipice of a 14% correction. The 2021 purchases happened right as the market was entering a bear market, which saw the S&P fall 25% before

bottoming in October 2022

.

I am literally the unluckiest market timer I know.

Fortunately, my full-time job is researching the data and writing about having exposure to stocks during the market’s ups and downs. It’s helped me keep my investment decisions very informed.

I also have a carefully thought-out personalized financial strategy that takes into account the risk of big drawdowns. Importantly, I have a time horizon that allows me to ride out the downturns as I build wealth for the long run.

Thanks to having good financial information and a good financial plan, I held on.

And today, those older very

poorly timed trades

are in the black, and they’re helping me get closer to achieving my long-term financial goals.

The S&P 500 is up about 170% since my late 2015 purchase.

And it’s up about 20% since my late 2021 and early 2022 purchases.

As Bespoke’s Paul Hickey

says

: "Time heals in the markets."

Timing the market like Warren Buffett 👯♀️

Like billionaire investor Warren Buffett

, I don’t claim to be good at timing the stock market. (Buffett receives praise for writing a widely circulated op-ed titled “Buy American” during the global financial crisis. Though, he published it in Oct. 2008 before the S&P fell another 26%.)

Fortunately, you don’t have to be a good market timer to be a successful investor. You just have to be able to

put in the time

.

The stock market will test an investor’s mettle. Below is an excerpt from the

January 23, 2022, TKer

:

…Investing in the stock market is a challenging mental exercise.

Among other things, investors have to cope with two seemingly conflicting realities: In the long-run, things almost always work out for the better; but in the short-run, anything and everything can go very badly.

In an environment where news headlines seem overwhelmingly alarming, I think it’s helpful for investors to see what history says about the market implications of comparable events. And as you’ll read on

TKer

, there’s nothing that the stock market couldn’t overcome

given enough time

.

HOWEVER

, it can’t be reiterated enough that 5% pullbacks and 10% corrections

happen more often than not

in any given year. Bear markets, where stocks fall by more than 20% from their highs, are less frequent, but they are something that long-term investors are likely to confront during their investment time horizons.

Unfortunately, it is incredibly difficult to predict when stocks will fall. And exiting stocks in an attempt to avoid short-term losses can prove

incredibly costly to long-term returns

.

So, whether or not you can comprehensively identify and balance all of the potential bullish and bearish market catalysts, it’s probably a good idea to just always be prepared for stocks to experience some big dips on their long upward journey…

There were several notable data points and macroeconomic developments since our

last review

:

🏛️

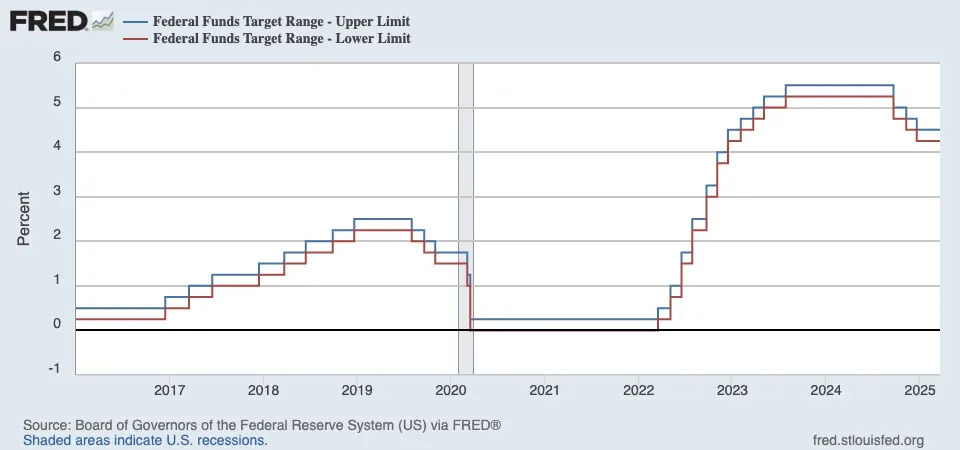

The

Fed keeps rates unchanged as expected

. In its

monetary policy announcement

on Wednesday, the Federal Reserve left its target for the federal funds rate unchanged at a range of 4.25% to 5.5%.

From the Fed’s

policy statement

: "Recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate has stabilized at a low level in recent months, and labor market conditions remain solid. Inflation remains somewhat elevated. The Committee seeks to achieve maximum employment and inflation at the rate of 2% over the longer run. Uncertainty around the economic outlook has increased. The Committee is attentive to the risks to both sides of its dual mandate."

The committee also reduced its

projections

for GDP growth while raising projections for inflation in the near-term.

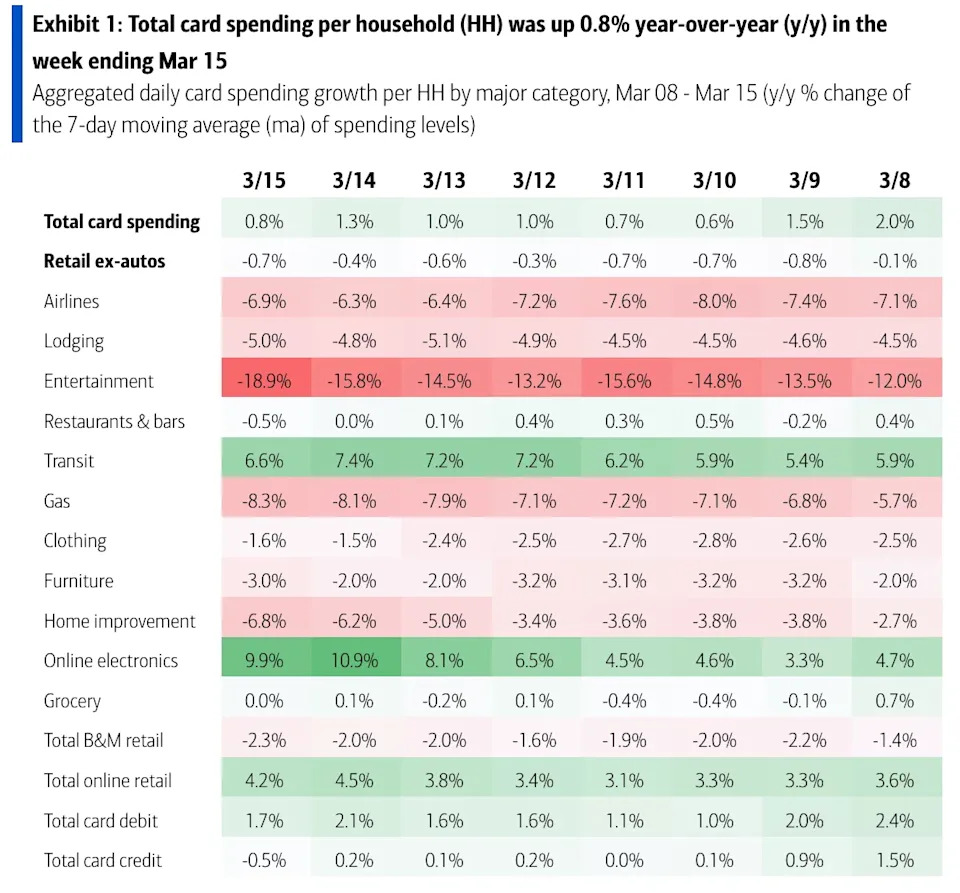

💳

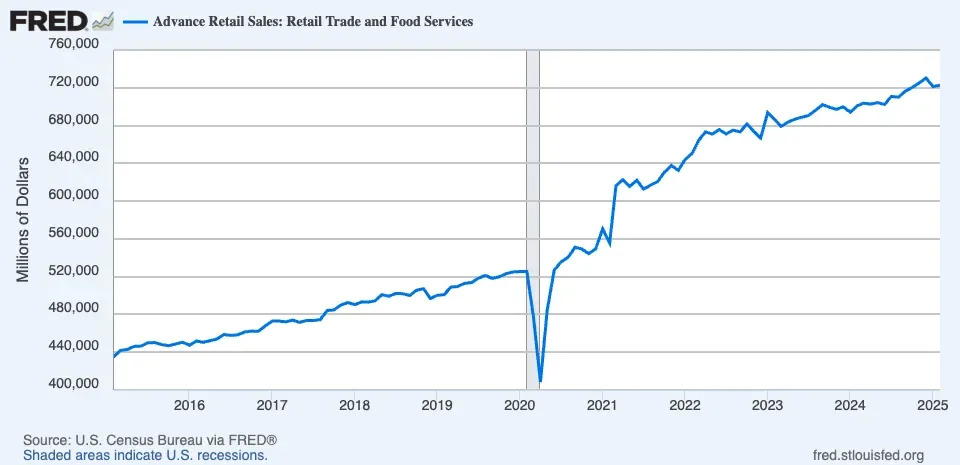

Card spending data is holding up

. From JPMorgan: "As of 14 Mar 2025, our Chase Consumer Card spending data (unadjusted) was 2.5% above the same day last year. Based on the Chase Consumer Card data through 14 Mar 2025, our estimate of the US Census March control measure of retail sales m/m is 0.47%."

From BofA: "Total card spending per HH was up 0.8% y/y in the week ending Mar 15, according to BAC aggregated credit & debit card data. Among the categories we show, the biggest slowdowns relative to the week ending Mar 8 were in entertainment and HI. Meanwhile, the biggest gain was in online electronics."

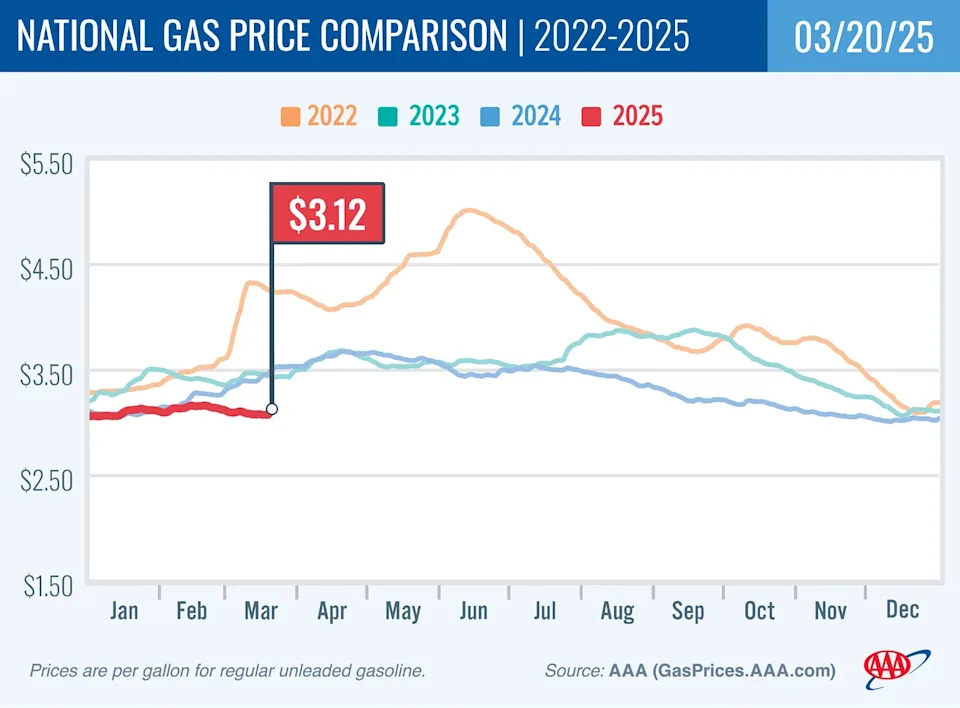

⛽️

Gas prices tick higher

. From

AAA

: "After weeks of little movement, the national average for a gallon of gas increased by about 4 cents since last week to $3.12. Even though the price of crude oil remains below $70 a barrel, prices at the pump are going up as more refineries make the seasonal switch to summer-blend gasoline. Summer-blend gas is less likely to evaporate in warmer temperatures and is more expensive to produce."

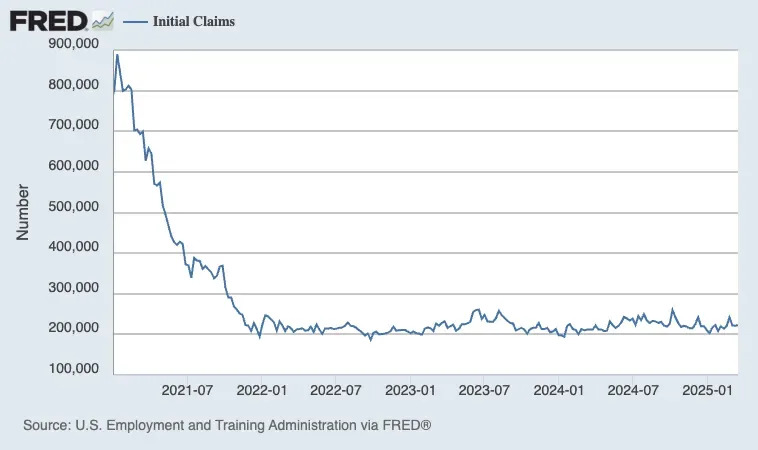

💼

Unemployment claims tick higher

.

Initial claims for unemployment benefits

rose to 223,000 during the week ending March 15, up from 221,000 the week prior. This metric continues to be at levels historically associated with economic growth.

Federal layoffs brought by the Trump administration’s Department of Government Efficiency appear making their way into the data. Initial claims filed by federal employees came in at 1,580 in the week ending March 1.

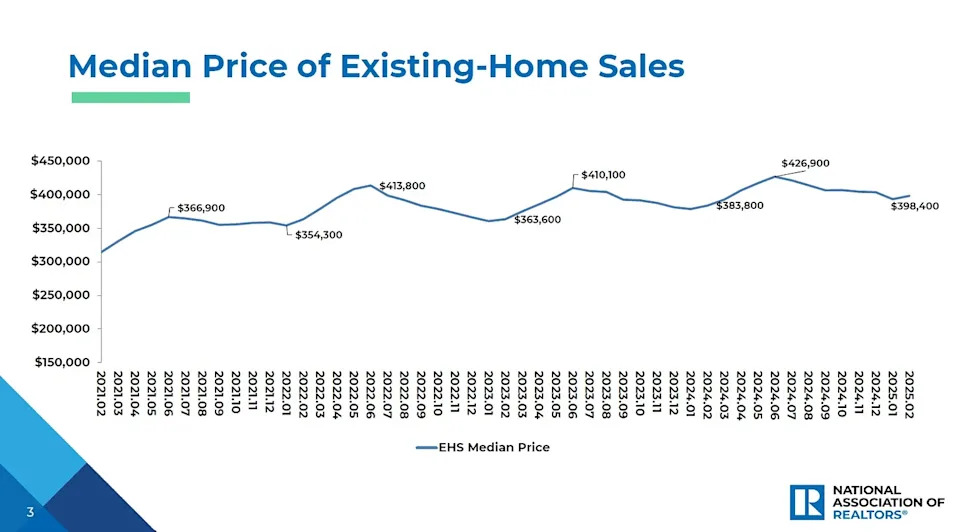

🏚 Home sales rise

.

Sales of previously owned homes

increased by 4.2% in February to an annualized rate of 4.26 million units. From NAR chief economist Lawrence Yun: "Home buyers are slowly entering the market. Mortgage rates have not changed much, but more inventory and choices are releasing pent-up housing demand."

🏠

Mortgage rates tick higher

. According to

Freddie Mac

, the average 30-year fixed-rate mortgage rose to 6.67% from 6.65% last week. From Freddie Mac: "The 30-year fixed-rate mortgage has stayed under 7% for nine consecutive weeks, which is helpful for potential buyers and sellers alike."

🏠

Homebuilder sentiment falls.

From the

NAHB’s Carl Harris

: “Builders continue to face elevated building material costs that are exacerbated by tariff issues, as well as other supply-side challenges that include labor and lot shortages.”

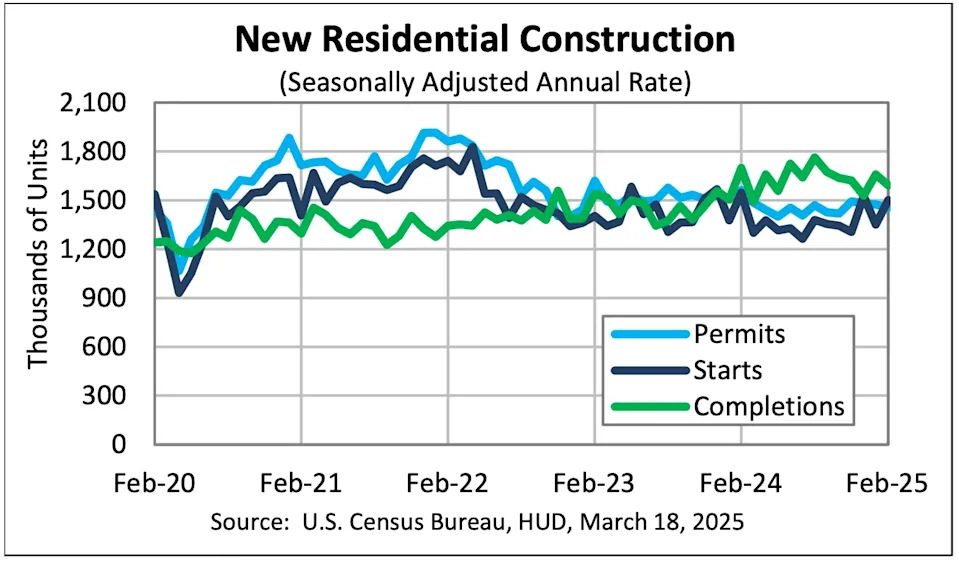

🔨

New home construction starts rise

. Housing starts grew 11.2% in February to an annualized rate of 1.5 million units, according to

the Census Bureau

. Building permits ticked down 1.2% to an annualized rate of 1.46 million units.

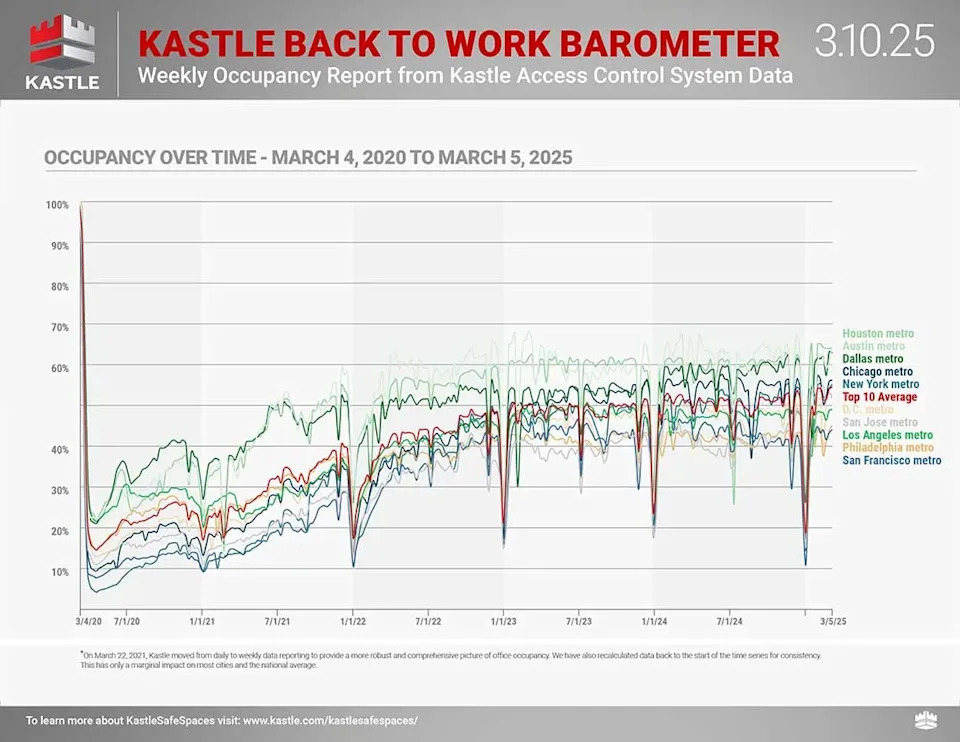

🏢

Offices remain relatively empty

. From

Kastle Systems

: "Peak day office occupancy was 62.9% on Tuesday last week, down half a point from the previous week. Most cities experienced more losses than gains, as three out of five days had lower overall occupancy than last week. Washington, D.C., however, saw higher occupancy every day of the week, matching its post-pandemic record high of 63.1% on Tuesday. And Chicago had higher occupancy on four out of five days, peaking at 71.8% on Tuesday. The average low was on Friday at 36.4%, the same as last week."

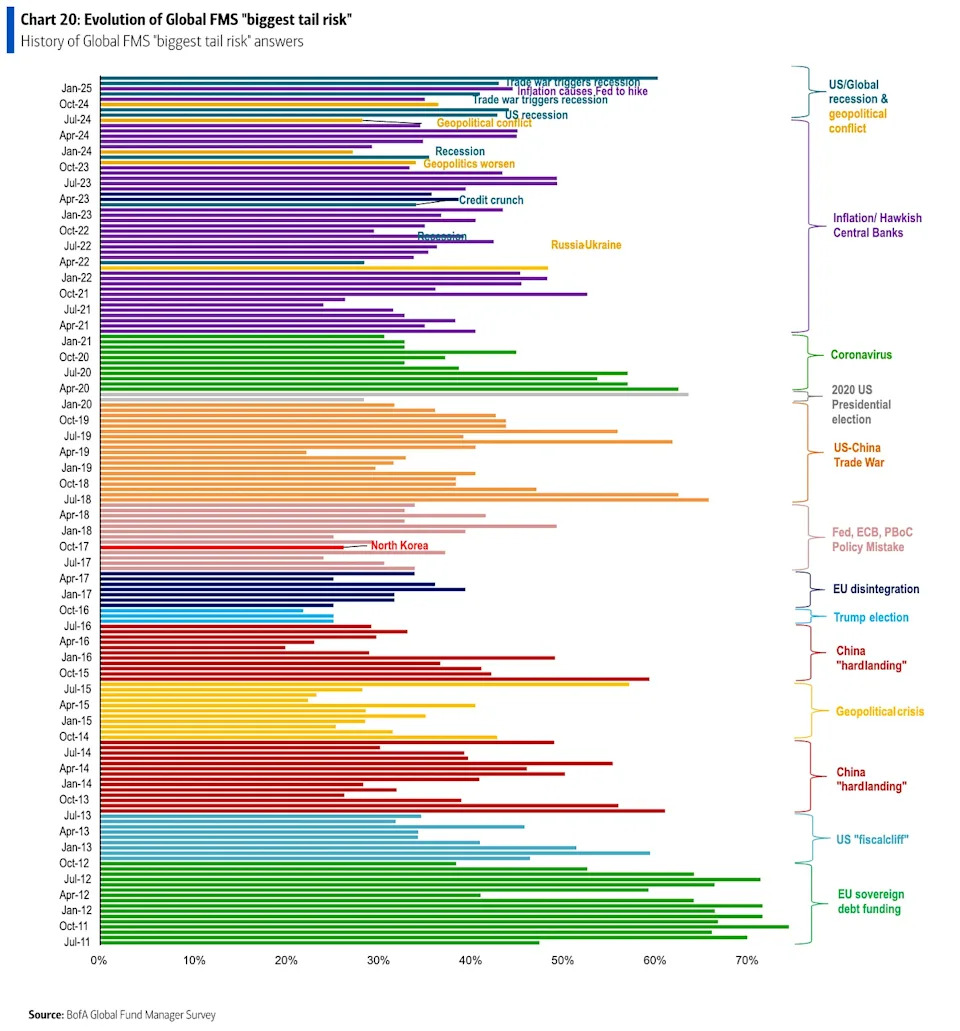

😬

This is the stuff pros are worried about

. According to BofA’s March Global Fund Manager Survey: "On tail risks…55% of March FMS investors say a recessionary trade war is the biggest 'tail risk', the highest 'tail risk' conviction since "Covid resurgence" in Apr'20."

Actions speak louder than words

: We are in an odd period given that the hard economic data has

decoupled from the soft sentiment-oriented data

. Consumer and business sentiment has been relatively poor, even as tangible consumer and business activity continue to grow and trend at record levels. From an investor’s perspective,

what matters

is that the hard economic data continues to hold up.

Think long term

: For now, there’s no reason to believe there’ll be a challenge that the economy and the markets

won’t be able to overcome

over time.

The long game remains undefeated

, and it’s a streak long-term investors can expect to continue.