3 Reasons to Sell TMO and 1 Stock to Buy Instead

Over the last six months, Thermo Fisher shares have sunk to $508.90, producing a disappointing 17.1% loss - worse than the S&P 500’s 1.2% drop. This might have investors contemplating their next move.

Is now the time to buy Thermo Fisher, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free .

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons why we avoid TMO and a stock we'd rather own.

Why Is Thermo Fisher Not Exciting?

Known for its involvement in the Human Genome Project, Thermo Fisher (NYSE:TMO) supplies instruments, laboratory equipment, and reagents for scientific research and healthcare.

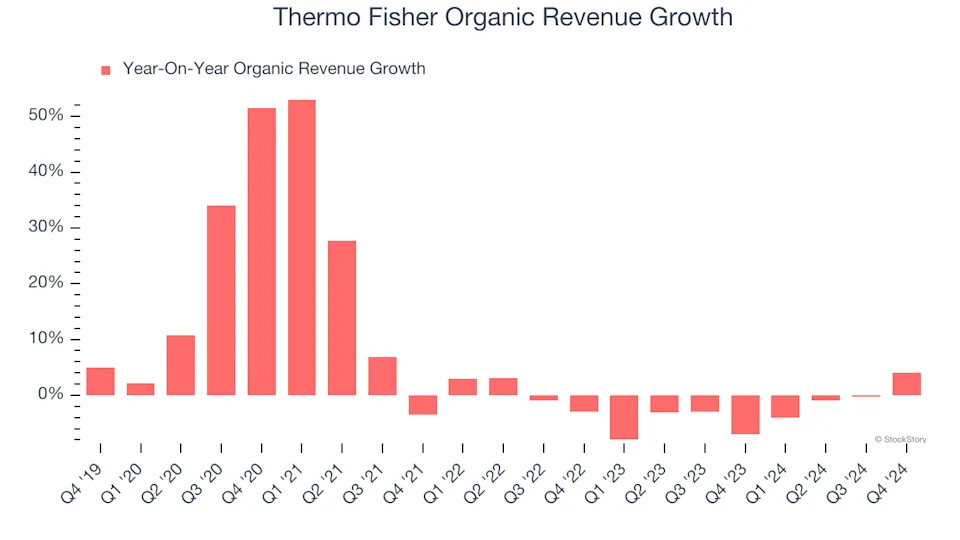

1. Core Business Falling Behind as Demand Declines

In addition to reported revenue, organic revenue is a useful data point for analyzing Research Tools & Consumables companies. This metric gives visibility into Thermo Fisher’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Thermo Fisher’s organic revenue averaged 2.8% year-on-year declines. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests Thermo Fisher might have to lean into acquisitions to grow, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

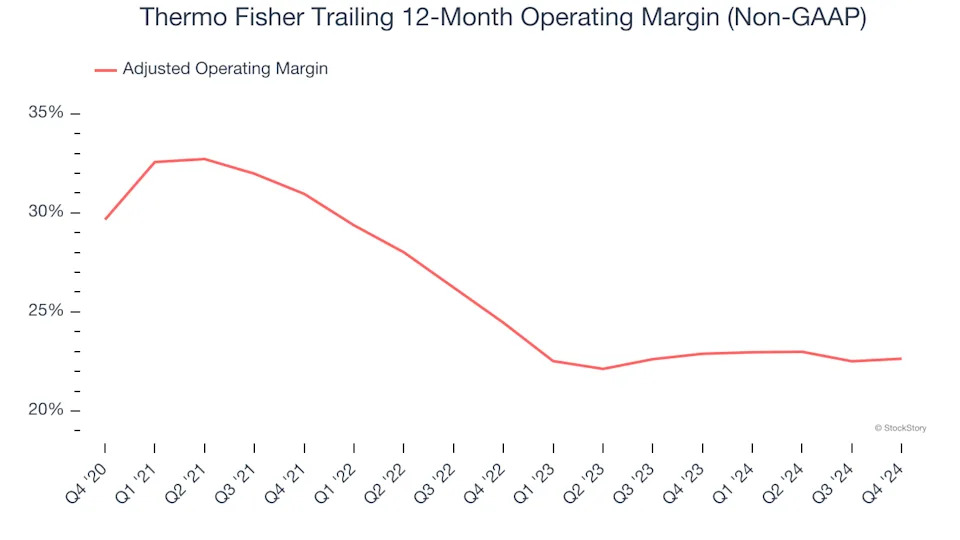

2. Shrinking Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Analyzing the trend in its profitability, Thermo Fisher’s adjusted operating margin decreased by 7 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its adjusted operating margin for the trailing 12 months was 22.6%.

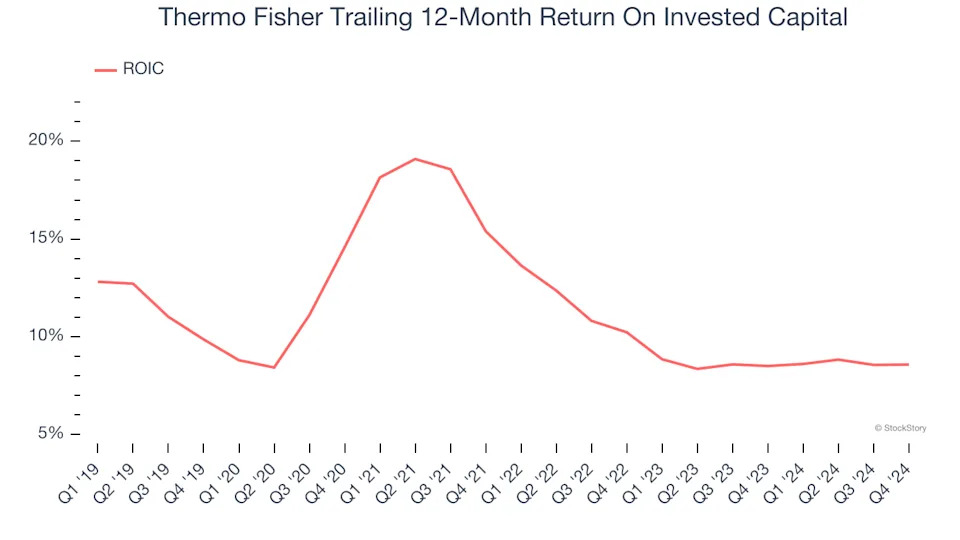

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).