Manufacturing is the basis of the global economy. Almost everything, from footwear to automobiles, is produced in factories. Within that landscape,

Fastenal

(NASDAQ: FAST)

has built a tremendous business.

The company distributes fasteners, supplies, safety gear, and other products that almost every manufacturer needs but often overlooks.

Decades of steady growth have made Fastenal a giant in the industry, and its shareholders quite wealthy. The company has paid and raised its dividend for 25 consecutive years, and returned over 13,000% since the mid-1990s.

Shares are up 67% over the past three years alone. Can the stock continue to deliver, or is Fastenal approaching the end of its runway? Here is what you need to know.

Innovation and a convenience-focused value proposition have fueled Fastenal's success

Supply chains are crucial to all manufacturers. But while most companies focus on the core materials they need to build their products, they often overlook the simple items that workers frequently need. Think nuts and bolts, safety goggles, and batteries. Fastenal has found immense success catering to this need.

Fastenal is a leading distributor of industrial supplies, selling essential yet under-the-radar products to its customers. It focuses on technology to provide excellent service and nearly unbeatable convenience.

For example, Fastenal installs vending machines at customer facilities, allowing workers to easily access what they need without interrupting their work. Fastenal will also open on-site stores at larger facilities and has a full-fledged e-commerce storefront.

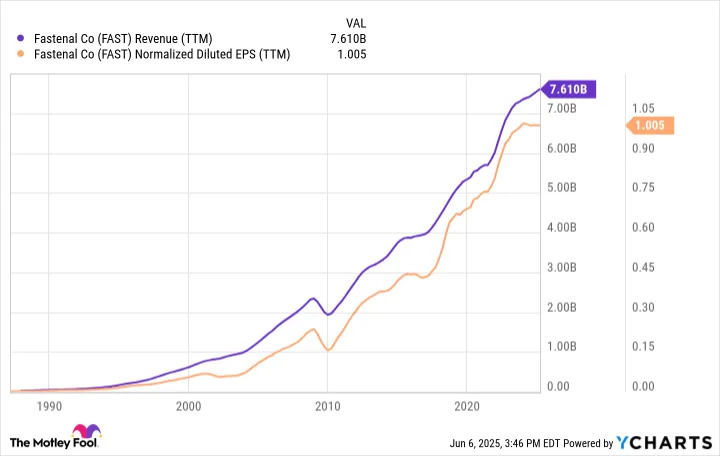

Continuous expansion has helped Fastenal continue to grow its top and bottom lines:

A diversified, growing revenue base funds a rising dividend

Today, Fastenal has approximately 130,000 vending machines installed, up from 55,000 in 2015. It seems clear that Fastenal's business model is effective, so it's more a matter of how long the company can sustain its expansion.

Most manufacturing sites are small, making vending machines a great solution. Fastenal's installed vending base grew by 12.2% from 2023 to 2024 and by 12.4% year over year in Q1 2025, so its growth momentum remains strong. Management estimates that its addressable market could support upward of 1.7 million units.

Fastenal also works with national accounts, which often buy more but have more complex needs. The company signs contracts with these customers. In 2024, national accounts represented 63% of total sales. However, no single customer contributed more than 5% of Fastenal's sales last year, so there is little risk of painful fallout if any given customer were to leave.

Such a diverse business enables Fastenal to continue paying and increasing its dividend. The company has raised its payout through both the 2007-2009 financial crisis and the COVID-19 pandemic, two of the worst scenarios for its industrial-focused customer base in decades.

The

dividend payout ratio

is higher than you'd like to see in most industrial stocks, at 80% of earnings. However, Fastenal doesn't spend much on

capital expenditures

, and the business has zero net debt. Management has raised the dividend at an annualized rate of 12% over the past decade, and occasionally pays a special dividend.

Fastenal's willingness to return cash to shareholders is a significant contributor to the stock's long-term results.

Is it too late to buy Fastenal stock?

Wall Street also seems to think that Fastenal will continue to sustain solid growth. Analysts estimate the company will grow earnings by an average of just over 10% annually over the long term.

That doesn't mean the stock is without risks. Much of what Fastenal sells comes from non-U.S. sources, which means tariffs could weigh on the business if they persist. Additionally, Fastenal's business would be affected during a recession, as the company's manufacturing-driven customer base would likely slow.

But while Fastenal's future appears bright, the stock's valuation already reflects that. The stock's success has pushed its price-to-earnings (P/E) ratio to 42, which is a bit high for a business with an expected 10% earnings growth rate.

That values the stock at a PEG ratio of about 4.0, and I generally shy away from buying high-quality stocks above PEG ratios of 2.0 to 2.5. The risk of downside if something goes wrong becomes uncomfortably high as you start going beyond that.

So it's not too late to be bullish on Fastenal, but investors would be wise to wait for a lower price before scooping up shares.

Should you invest $1,000 in Fastenal right now?

Before you buy stock in Fastenal, consider this:

The

Motley Fool Stock Advisor

analyst team just identified what they believe are the

10 best stocks

for investors to buy now… and Fastenal wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when

Netflix

made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation,

you’d have $669,517

!*

Or when

Nvidia

made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation,

you’d have $868,615

!*

Now, it’s worth noting

Stock Advisor

’s total average return is

792% — a market-crushing outperformance compared to

173%

for the S&P 500. Don’t miss out on the latest top 10 list, available when you join

Stock Advisor

.

Justin Pope

has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a

disclosure policy

.