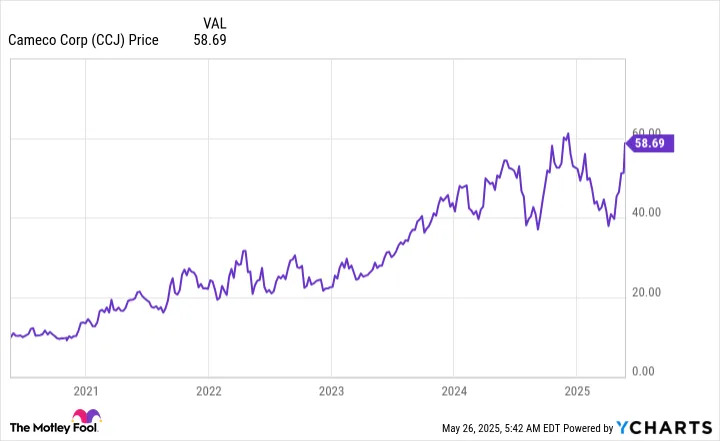

After the Fukushima nuclear meltdown in Japan in 2011, shares of uranium miner

Cameco

(NYSE: CCJ)

fell into a deep rut. It took a decade for it to climb out of the hole, and in 2024, the stock rose toward a high of a little over $60 a share on rising uranium prices.

When uranium prices began falling in February 2024, the stock fell along with it, going as low as the mid-$30s. The stock price eventually recovered and it now trades around $58 a share.

Should investors buy Cameco as it makes a run toward the 25-year-high price of a touch over $60 again?

What does Cameco do?

Cameco is a large Canadian miner that produces and processes uranium into

fuel for nuclear power

plants. It also owns a 49% stake in Westinghouse, which provides services -- from plant construction to plant maintenance -- to nuclear power companies. It is one of the largest publicly traded producers of uranium on the planet.

A key selling point for Cameco's uranium is where it operates. The vast majority of its owned mines are in North America, a region considered economically and politically stable. And while it does source uranium from less-stable regions, potential customers generally appreciate working with companies from stable regions.

Cameco's long history in the industry is another positive, since it proves the company can survive the swings that commodities often experience.

Such swings are particularly notable for uranium because external factors can have such a large effect on the nuclear power industry. The Fukushima meltdown was the most recent example, with other notable events including Three Mile Island and Chernobyl. After such high-profile disasters, nuclear power usually goes through a period in which it is shunned and uranium prices fall.

The nuclear renaissance, this time around

When nuclear power is out of favor and uranium demand is thus relatively weak, Cameco's stock price suffers. But nuclear power is increasingly being seen as a clean source of baseload power (the minimum required to meet the demands of a power grid) to support intermittent clean energy sources like

solar and wind

. With Fukushima more than a decade in the past, the negative overhang is long over.

Despite a year-over-year drop in uranium prices, Cameco managed to put up solid first-quarter 2025 earnings results. That's in large part because it doesn't sell uranium at the spot price, it signs long-term contracts.

This helps support earnings when uranium prices are falling, but it can hinder earnings when uranium prices are rising. All in, more conservative investors will likely view this approach as a fair trade-off given that uranium is an often volatile commodity.

That said, it is the long-term story that investors will want to consider if they are looking at Cameco right now. That's because, based on current expectations, there is going to be a growing supply gap starting in 2030.

The increasing use of nuclear power around the world is causing that gap, and if nothing changes, uranium will likely become more dear in a few years. And that should lead to increasingly strong results for Cameco.

Should you buy Cameco now, as it gets back to its $60-ish highs?

Cameco is a supplier to the nuclear power industry, making it a pick-and-shovel play on the growth of this energy source. Given its use of long-term contracts, it is one of the less volatile ways to invest in uranium. And the long-term outlook for uranium demand suggests that strong financial performance is likely as uranium demand rises above supply.

All of this makes Cameco look attractive today if you have a glass-half-full view of the world.

The glass-half-empty view here, which deserves strong consideration, is that past nuclear power renaissances haven't lasted. The big problem is that the view of nuclear power could change quickly if there is another power plant meltdown. And with Cameco's stock heading back toward 25-year highs, there's more downside than there has been in a long time for what is still a commodity-driven business.

In other words, only more aggressive investors with a positive view of uranium should consider Cameco. Most others will probably be better off sticking to a utility company that owns nuclear power plants, like

Southern Company

or

Constellation Energy

.

Should you invest $1,000 in Cameco right now?

Before you buy stock in Cameco, consider this:

The

Motley Fool Stock Advisor

analyst team just identified what they believe are the

10 best stocks

for investors to buy now… and Cameco wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when

Netflix

made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation,

you’d have $651,049

!*

Or when

Nvidia

made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation,

you’d have $828,224

!*

Now, it’s worth noting

Stock Advisor

’s total average return is

979% — a market-crushing outperformance compared to

171%

for the S&P 500. Don’t miss out on the latest top 10 list, available when you join

Stock Advisor

.

Reuben Gregg Brewer

has positions in Southern Company. The Motley Fool has positions in and recommends Constellation Energy. The Motley Fool recommends Cameco. The Motley Fool has a

disclosure policy

.