Deckers’s (NYSE:DECK) Q1 Sales Beat Estimates But Stock Drops 13%

May 22, 2025

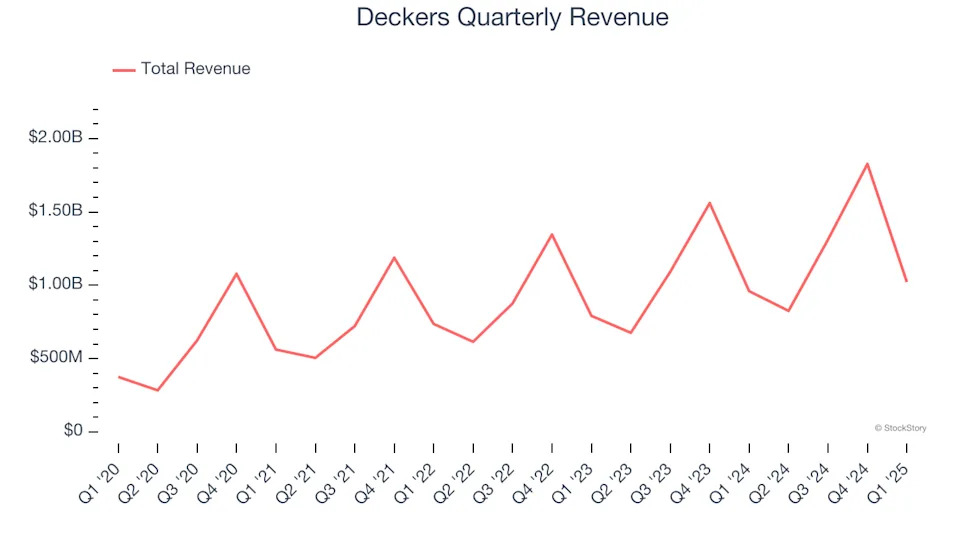

Footwear and apparel conglomerate Deckers (NYSE:DECK) announced better-than-expected revenue in Q1 CY2025, with sales up 6.5% year on year to $1.02 billion. On the other hand, next quarter’s revenue guidance of $900 million was less impressive, coming in 2.1% below analysts’ estimates. Its GAAP profit of $1 per share was 65.1% above analysts’ consensus estimates.

“Deckers delivered another exceptional year of results in fiscal 2025, highlighted by the HOKA and UGG brands’ respective revenue growth of 24% and 13%, as well as record earnings per share,” said Stefano Caroti, President and Chief Executive Officer.

Company Overview

Established in 1973, Deckers (NYSE:DECK) is a footwear and apparel conglomerate with a portfolio of lifestyle and performance brands.

Sales Growth

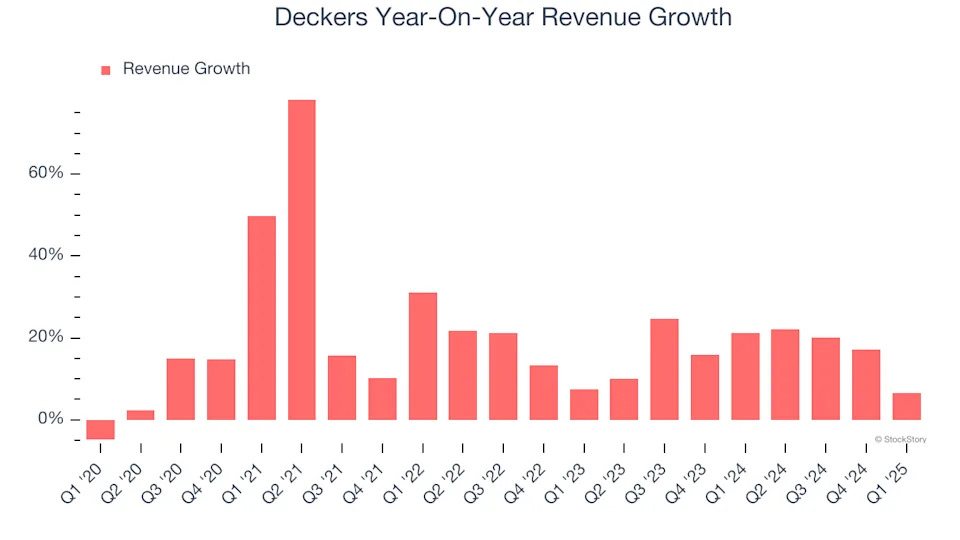

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Deckers grew its sales at a solid 18.5% compounded annual growth rate. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Deckers’s annualized revenue growth of 17.2% over the last two years is below its five-year trend, but we still think the results were respectable.

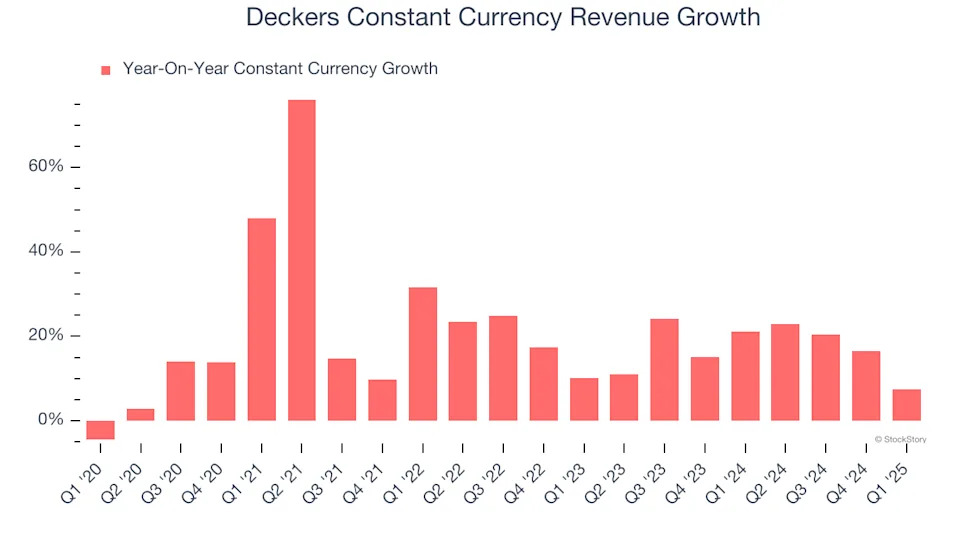

We can better understand the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 17.4% year-on-year growth. Because this number aligns with its normal revenue growth, we can see that Deckers has properly hedged its foreign currency exposure.

This quarter, Deckers reported year-on-year revenue growth of 6.5%, and its $1.02 billion of revenue exceeded Wall Street’s estimates by 2.4%. Company management is currently guiding for a 9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.5% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI.

Click here to access our free report one of our favorites growth stories

.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Deckers’s operating margin has risen over the last 12 months and averaged 22.8% over the last two years. On top of that, its profitability was elite for a consumer discretionary business, showing it’s a well-oiled machine with an efficient cost structure that benefits from operating leverage as it scales.

In Q1, Deckers generated an operating profit margin of 17%, up 1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

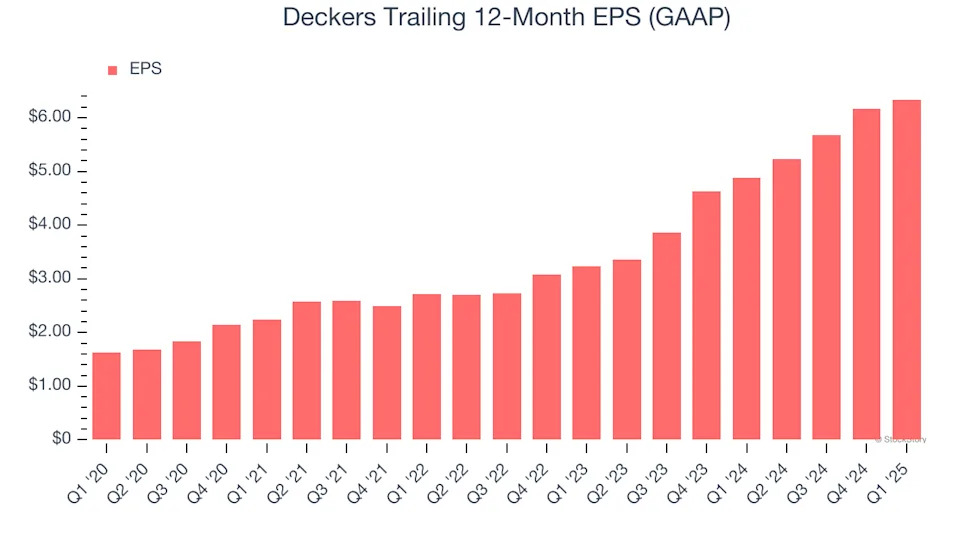

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Deckers’s EPS grew at an astounding 31.3% compounded annual growth rate over the last five years, higher than its 18.5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q1, Deckers reported EPS at $1, up from $0.83 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Deckers’s full-year EPS of $6.34 to stay about the same.

Key Takeaways from Deckers’s Q1 Results

We liked that Deckers beat analysts’ constant currency revenue expectations this quarter. We were also excited its EPS outperformed Wall Street’s estimates. On the other hand, both revenue and EPS guidance for next quarter missed. Zooming out, we think this was a mixed quarter, and the guidance will weigh on shares. The stock traded down 12.9% to $109.99 immediately following the results.