Altria vs. Philip Morris: Which Tobacco Stock Is a Better Buy Now?

May 20, 2025

In the world of tobacco investing,

Altria Group, Inc.

MO and

Philip Morris International Inc.

PM stand out as two of the most dominant players. While they share a common legacy, their strategies have diverged in recent years. Altria remains focused on the U.S. market, where it continues to dominate in traditional cigarettes while gradually expanding into reduced-risk products (RRPs). Philip Morris, in contrast, is leading a global transformation, aggressively expanding its heated tobacco portfolio and advancing its smoke-free future strategy.

For investors comparing these two tobacco giants, the real question is: Which stock has greater long-term growth potential, and how well is each company executing its transition from traditional tobacco to next-generation products?

One-Year Price Performance

Image Source: Zacks Investment Research

The Case for Altria

Altria, the company behind Marlboro in the United States, stands at a pivotal moment in its history. With smoking rates in long-term decline and nicotine preferences rapidly shifting, the company faces growing pressure to move beyond its cigarette-heavy roots. While Altria still commands over 40% of the U.S. cigarette market, cigarette volumes continue to shrink, and pricing power — a key buffer for years — is beginning to lose effectiveness amid inflation and growing consumer price sensitivity. In the first quarter of 2025, its Smokeable Products’ net revenues fell 5.8% to $4,622 million due to reduced shipment volume.

The broader tobacco landscape is clearly evolving, and for Altria, the urgency to accelerate its transition into RRPs has never been greater. To address this shift, it is building a smoke-free portfolio, focusing on modern oral nicotine and vapor products. Through its subsidiary Helix Innovations, Altria owns 100% of on!, a tobacco-derived nicotine pouch that is gaining traction with U.S. consumers. In the first quarter, shipment volumes for on! grew 18% year over year, despite higher prices at retail. This growth reflects rising consumer acceptance and brand equity, though the competitive environment remains intense. Swedish Match, owned by Philip Morris, continues to expand in the category, making the race for the share in modern oral both fast-moving and crowded.

Meanwhile, Altria’s efforts in the e-vapor space have faced more significant headwinds. The company was recently forced to pull NJOY ACE from the market following a regulatory challenge. The setback has disrupted near-term momentum, but Altria remains committed to the vapor category. It has called out the growing share of illicit disposable vapes, which now make up over 60% of the e-vapor market and pose a direct threat to authorized products like NJOY. Despite these challenges, Altria views the situation as an opportunity to innovate, with plans to use NJOY’s R&D capabilities to develop next-generation, compliant vapor products that can better meet consumer demand.

Unlike its global peers, Altria is fully concentrated in the U.S. market — an advantage in terms of operational focus, but a liability in an increasingly restrictive regulatory climate. With potential menthol bans, nicotine caps, and flavor restrictions on the horizon, it is operating in a tightening environment that limits innovation and slows product adoption. This domestic-only exposure increases the complexity and cost of execution, leaving Altria with less room for error as it navigates its transformation.

The Case for Philip Morris

Philip Morris is setting a new industry benchmark in the global shift toward a smoke-free future. At the heart of this transformation is IQOS, PMI’s flagship heat-not-burn device, which has emerged as a leading RRP. IQOS continues to gain strong traction in key international markets, including Japan and several parts of Europe, as adult smokers seek better alternatives to traditional cigarettes.

Unlike many competitors still reliant on combustible tobacco products, Philip Morris is reinventing its core business through investments in science-based alternatives designed to help adult smokers transition away from smoking. In 2022, PM further strengthened its smoke-free product portfolio with the acquisition of Swedish Match, securing a strong position in the rapidly expanding oral nicotine segment. This strategic move complements IQOS and has broadened PMI’s offerings with popular products like ZYN nicotine pouches and General snus.

This transformation is already delivering results. In the first quarter of 2025, smoke-free products contributed 42% of the company’s total revenues and 44% of gross profit. The segment saw a 15% year-over-year revenue increase. IQOS maintained its leadership in the inhalable smoke-free category, while ZYN continued to gain market share, with rising shipment volumes in the oral nicotine market. At the same time, the company continues to demonstrate strength in its traditional combustible tobacco business, which achieved organic revenue growth of 3.8% in the first quarter. This highlights the company’s ability to manage its legacy operations while accelerating the shift toward RRPs.

What sets Philip Morris apart is its ability to combine cutting-edge product innovation with strong regulatory credibility. Unlike MO, which operates within the U.S. market, PMI’s global footprint enables it to tap into diverse international markets, unlocking broader growth opportunities and allowing for better regulatory risk diversification. While challenges such as currency volatility and geopolitical uncertainty persist, these are balanced by PM’s robust pipeline of smoke-free innovations, its well-established brand equity, and growing presence in the global RRP space.

How Does the Zacks Consensus Estimate Compare for PM & MO?

The Zacks Consensus Estimate for Philip Morris’ 2025 earnings per share (EPS) has moved up 3.3% over the last 30 days to $7.47, signaling a projected year-over-year increase of 13.7%. In comparison, the consensus EPS estimate for Altria has moved up 1.3% to $5.35 during the same period and points to growth of 4.5% for 2025. This comparison highlights a more optimistic profitability outlook for PM relative to MO.

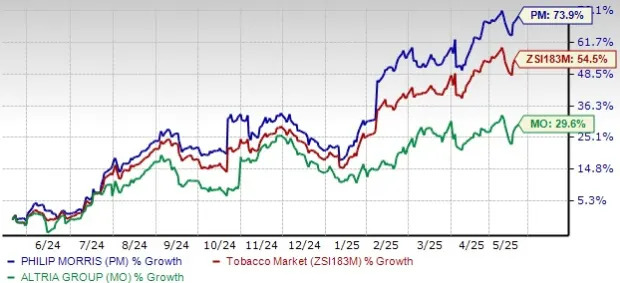

Price Performance of PM & MO

Philip Morris currently trades at a forward 12-month P/E of 22.20x while Altria trades at a lower multiple of 10.97. While PM’s valuation looks richer, investors are paying for visibility into a transformation that is already underway.

Image Source: Zacks Investment Research

Backing this valuation, Philip Morris’ stock has outperformed with a 73.9% gain over the past year, well ahead of Altria’s 29.6% and the industry’s 54.5%, highlighting investor confidence in its growth strategy.

Bottom Line

While both Altria and Philip Morris offer exposure to the evolving tobacco industry, PM stands out with its proven success in RRPs, global diversification and stronger earnings growth outlook. Altria’s U.S. market dominance remains appealing, but regulatory headwinds and a slower RRP transition limit its near-term upside. With a clearer smoke-free strategy, accelerating revenues from alternatives like IQOS and ZYN, and stronger stock performance, Philip Morris appears to be the better tobacco stock to buy for long-term growth.

PM currently has a Zacks Rank #1 (Strong Buy), while MO carries a Zacks Rank #3 (Hold). You can see

the complete list of today’s Zacks #1 Rank stocks here

.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report