Here's Why Hold Strategy is Apt for Imperial Oil Stock Now

May 16, 2025

Imperial Oil Limited

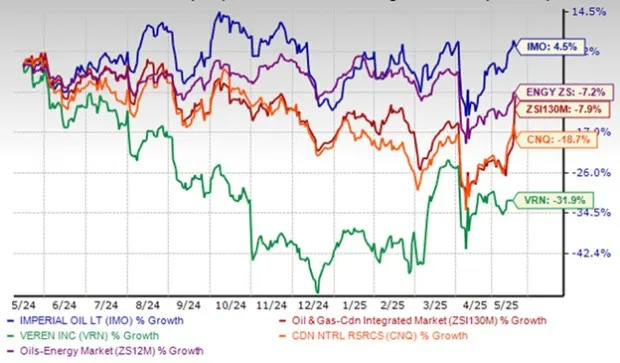

IMO has experienced a notable 3.3% increase in its share price over the past year, outperforming the broader oil and energy sector, which saw a decline of 7.2%. The company has also outpaced its competitors within the Canadian Oil and Gas Exploration and Production sub-industry, with

Cenovus Energy Inc.

CVE and

Canadian Natural Resources Limited

CNQ reporting declines of 32.5% and 19.8%, respectively, during the same time. Such relative strength naturally leads investors to ask: Is this a signal to buy now, or does patience offer a better entry point?

1-Year Price Comparison

Image Source: Zacks Investment Research

To answer this, it is important to understand the broader context behind Imperial’s momentum. Headquartered in Calgary, IMO is more than just a prominent Canadian oil company, it is a key industry player with a diverse portfolio spanning oil and gas production, refining, marketing and chemical manufacturing. As Canada's largest supplier of jet fuel and a top producer of asphalt, IMO holds a commanding presence in the market. Crucially, this strength is amplified by its deep strategic ties to

ExxonMobil

XOM, which holds a 69.6% ownership stake, providing IMO with access to global expertise, resources and technology.

Basically, the company makes revenues by exploring and extracting oil and gas, refining them into products like gasoline and diesel, and distributing these to its customer base.

But what exactly has driven its performance over the past year? Let us explore the key factors driving its success and evaluate whether this momentum can be maintained in the future.

Key Factors Boosting Imperial’s Market Position

Integrated Business Model Mitigates Downside Risks:

Unlike pure-play upstream producers, Imperial benefits from vertical integration, combining oil production (Upstream) with refining and marketing (Downstream). In the first quarter of 2025, Downstream earnings surged to C$584 million, up C$228 million from the fourth quarter of 2024, due to strong margin capture, offsetting softer Upstream volumes. This diversification provides resilience against oil price swings, as refining margins often improve when crude prices dip.

Shareholder-Friendly Capital Allocation:

Imperial has a proven track record of returning capital to its shareholders through dividends and share buybacks. In first-quarter 2025, the company paid C$307 million in dividends and announced plans to renew its Normal Course Issuer Bid, signaling confidence in future cash flows. Historically, Imperial has accelerated buybacks in the second half of the year, providing potential upside for investors. The company’s disciplined capital allocation, balancing growth investments (e.g., renewable diesel, Leming SAGD) with shareholder returns, enhances its appeal as a reliable income and growth stock.

Strategic Projects With a Renewable Edge:

Imperial is advancing key growth projects, including the Leming SAGD development at Cold Lake (expected to add 9,000 barrels per day at peak production) and the Strathcona renewable diesel facility, set to start in mid-2025. The renewable diesel project positions IMO as a leader in Canada’s low-carbon fuel transition, aligning with regulatory demands and consumer trends. Additionally, the Enhanced Bitumen Recovery Technology pilot at Aspen could unlock long-term, low-emission production growth. These initiatives demonstrate Imperial’s commitment to both traditional energy leadership and sustainable innovation.

Efficiency-Driven Cost Reductions:

Imperial has made strong progress in cutting costs and improving efficiency, especially at its Cold Lake and Kearl sites. At Cold Lake, the company has lowered its cash costs by more than C$3 per barrel in the first quarter year over year, due to the large part to the success of the Grand Rapids solvent-assisted SAGD (steam-assisted gravity drainage) project. Looking ahead, Imperial plans to reduce costs even further, targeting C$13 per barrel at Cold Lake and C$18 at Kearl.

One of the key steps toward this goal is optimizing maintenance schedules. At Kearl, for example, the company has doubled the time between major maintenance shutdowns from every two years to every four. This not only improves efficiency but also helps keep costs down. These efforts show that Imperial is well-positioned to remain profitable, even when oil prices are unpredictable.

Strategic Infrastructure Positioning:

Imperial benefits from its strategically located assets and integrated infrastructure across Canada. The company owns and operates key pipelines, storage facilities and transportation networks that provide reliable access to markets. This vertical integration helps mitigate midstream bottlenecks that often plague energy producers in Canada. With increasing global demand for reliable energy suppliers, Imperial's established infrastructure provides a durable competitive advantage.

Headwinds That Could Weigh on Imperial’s Outlook

Oil Price and Margin Volatility:

Despite strong operational execution, Imperial remains highly sensitive to fluctuations in crude oil prices and refining margins. In first-quarter 2025, the company reported that WTI crude oil prices averaged C$71.42 per barrel, down from C$76.86 in first-quarter 2024. While refining margins have improved year over year, they remain volatile and subject to macroeconomic uncertainty. Additional risks include trade tensions, such as potential U.S.-Canada tariffs. A significant decline in oil prices or a weakening of refining crack spreads could pressure Imperial’s earnings and cash flow, potentially affecting its capacity to maintain share buybacks and sustain dividend growth.

Operational Risks and Weather-Related Disruptions:

Imperial’s first-quarter production was impacted by extreme cold weather in February, with Kearl’s output falling to 256,000 barrels per day (down by 21,000 barrels year over year). While the company has improved cold-weather protocols, such events highlight the vulnerability of its operations to unforeseen disruptions. Unplanned downtime at Syncrude and maintenance-related throughput reductions in the Downstream segment (refinery utilization at 91% compared with 94% year over year) further highlight operational risks.

Lower Bitumen Prices Pressure Upstream Realizations:

Imperial experienced weaker realizations in its oil sands operations due to falling bitumen prices, impacting upstream margins. The narrowing of the WTI-WCS spread also added pressure. Unless Canadian heavy oil differentials improve, the company’s upstream earnings could remain under pressure, reducing the segment’s contribution to total profitability.

Heavy Reliance on Commodity Price Environment:

Despite downstream strength, Imperial’s earnings remain sensitive to commodity prices. Upstream profitability was significantly impacted by lower crude realizations in the first quarter. While downstream margins were strong, any reversal in refining economics or crude spreads could materially affect future performance, highlighting exposure to macro volatility.

Limited Exposure to LNG Growth:

Unlike some Canadian peers who are investing in Liquefied Natural Gas (“LNG”) export projects, Imperial remains focused almost exclusively on oil and refined products. This means the company may miss out on the growing global demand for natural gas as a transition fuel. The lack of LNG exposure could become a relative performance drag as global energy markets evolve.

Final Verdict on IMO Stock

Imperial benefits from a strong integrated business model, combining upstream production with downstream refining and marketing, which helps reduce the impact of oil price volatility. The company continues to deliver strong shareholder returns through dividends and share buybacks, while advancing key growth and renewable energy projects like the Strathcona renewable diesel facility. Cost reduction efforts and operational efficiency improvements, particularly at Cold Lake and Kearl, position Imperial for long-term profitability.

However, the company remains vulnerable to commodity price swings, with first-quarter 2025 upstream margins pressured by lower bitumen prices and WTI-WCS spreads. Additionally, operational risks like weather disruptions and limited exposure to LNG growth may hinder its ability to compete with more diversified peers in the evolving energy landscape.

Given this mix of strengths and potential challenges, investors should wait for a more opportune entry point instead of adding this Zacks Rank #3 (Hold) stock to their portfolios. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days.

Click to get this free report